At a time when countries around the world are shifting towards digital asset strategies, the UK has made it clear, it’s not following the crowd. During the Financial Times Digital Asset Summit in London, Emma Reynolds from the UK Treasury confirmed that the country will not copy the U.S. or the EU when it comes to creating a bitcoin reserve.

Let’s dive in detail!

No Plans to Hold Bitcoin as a Reserve

While the U.S. is thinking about holding Bitcoin as part of its reserves, with a neutral budget strategy, the UK has no plans to do the same.

UK Treasury, Reynolds said, “We don’t think that’s right for our market.” Instead of focusing on Bitcoin as a reserve, the UK is exploring new ways to use blockchain. One idea is to issue government debt using blockchain technology.

A process is already underway to find a supplier for this, with results expected by late summer.

Despite rejecting the U.S. model of holding Bitcoin, the UK still values cooperation with American regulators. Reynolds mentioned a new joint working group between UK and U.S. officials focused on crypto oversight. She said both sides agree that global collaboration is key in this fast-moving space.

No Copying the EU’s Crypto Rules

Reynolds also made it clear that the UK doesn’t want to copy the EU’s special crypto rules, known as MiCA. Reynolds said the UK has its way of making laws, which is more focused on outcomes rather than strict rules.

She explained that the UK plans to treat crypto companies like regular financial firms if they take on the same risks. This means, “Same risk, same rules.

Reynolds also admitted that some parts of crypto, like Bitcoin, are very hard for governments to control because they are fully decentralized. “There’s only so much we can do,” she said.

In short, the UK is choosing a balanced and practical way to manage crypto, fitting it into old rules, not creating brand-new ones.

Never Miss a Beat in the Crypto World!

Stay ahead with breaking news, expert analysis, and real-time updates on the latest trends in Bitcoin, altcoins, DeFi, NFTs, and more.

Earlier today, Israel launched a ‘pre-emptive strike’ on Tehran and declared a state of emergency. This rapid escalation of the conflict drove the crypto market into a freefall.

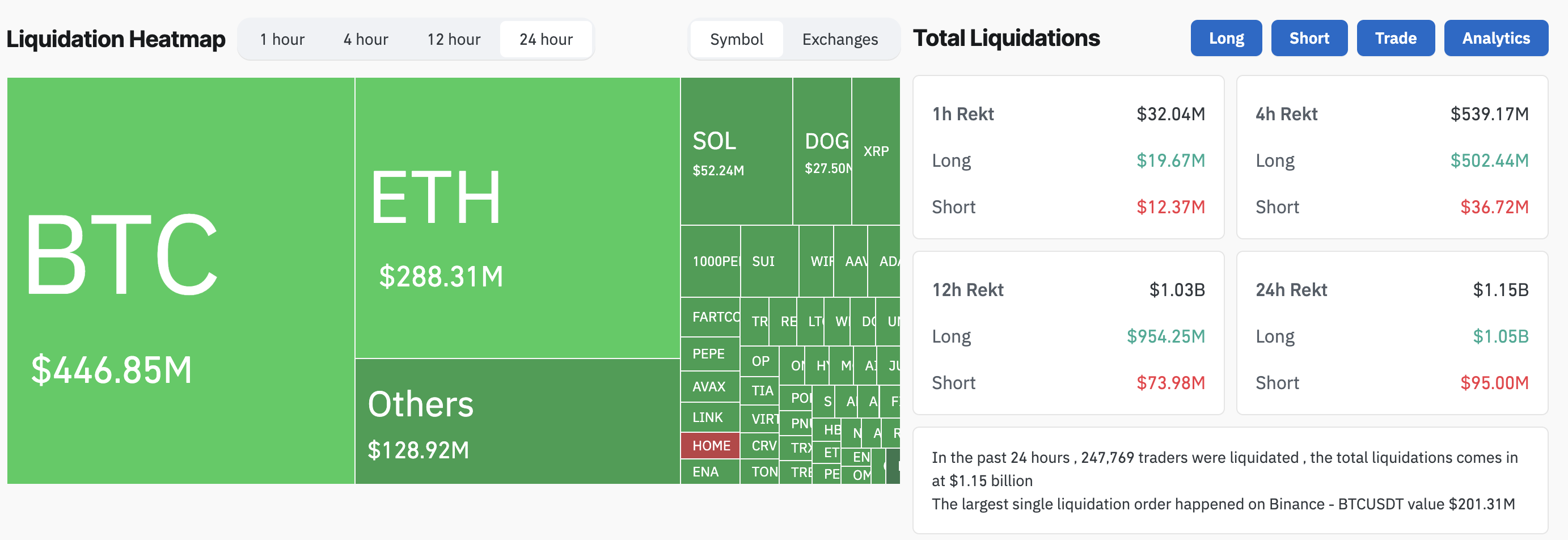

Over the past 24 hours, total liquidations amounted to $1.15 billion. Additionally, the overall market is down by 6.6%.

Crypto Market Plunges Amid Israel-Iran Conflict

According to CNN, Israel’s strikes targeted Iran’s nuclear program and missile capabilities, affecting dozens of locations. The attack reportedly eliminated Iran’s top military leaders and senior nuclear scientists. It was confirmed that General Hossein Salami, the Commander-in-Chief of Iran’s Islamic Revolutionary Guard Corps (IRGC), was killed.

“Iran’s state television says Deputy Commander in Chief of all Armed Forces, General Gholam Ali Rashid, has been killed, along with nuclear scientist Fereydoon Abbasi,” The Kobeissi Letter posted.

To prepare for potential retaliation, Israel has declared a state of emergency, closing schools, banning gatherings, and mobilizing tens of thousands of soldiers.

Furthermore, Iran is preparing a ‘lethal‘ response against Israel following the attacks. It has already appointed General Vahidi, the former head of the Quds Force, as the new commander of the IRGC.

Admiral Habibollah Sayyari has succeeded the late General Bagheri as the acting Commander-in-Chief of the Armed Forces of the Islamic Republic of Iran.

Statement No. 1 of the General Staff of the Armed Forces

In the early hours of Friday, 23 Khordad (June 12), the Zionist regime carried out an aggressive and reckless attack on several areas of the country, including both civilian and military zones. This assault resulted in… pic.twitter.com/TyQtkxPMmU

The rising tension between the two nations has caused significant turbulence in the market. Dow Jones Industrial Average futures fell by 1.3%, S&P 500 futures dropped 1.4%, and Nasdaq 100 futures plunged by 1.6%.

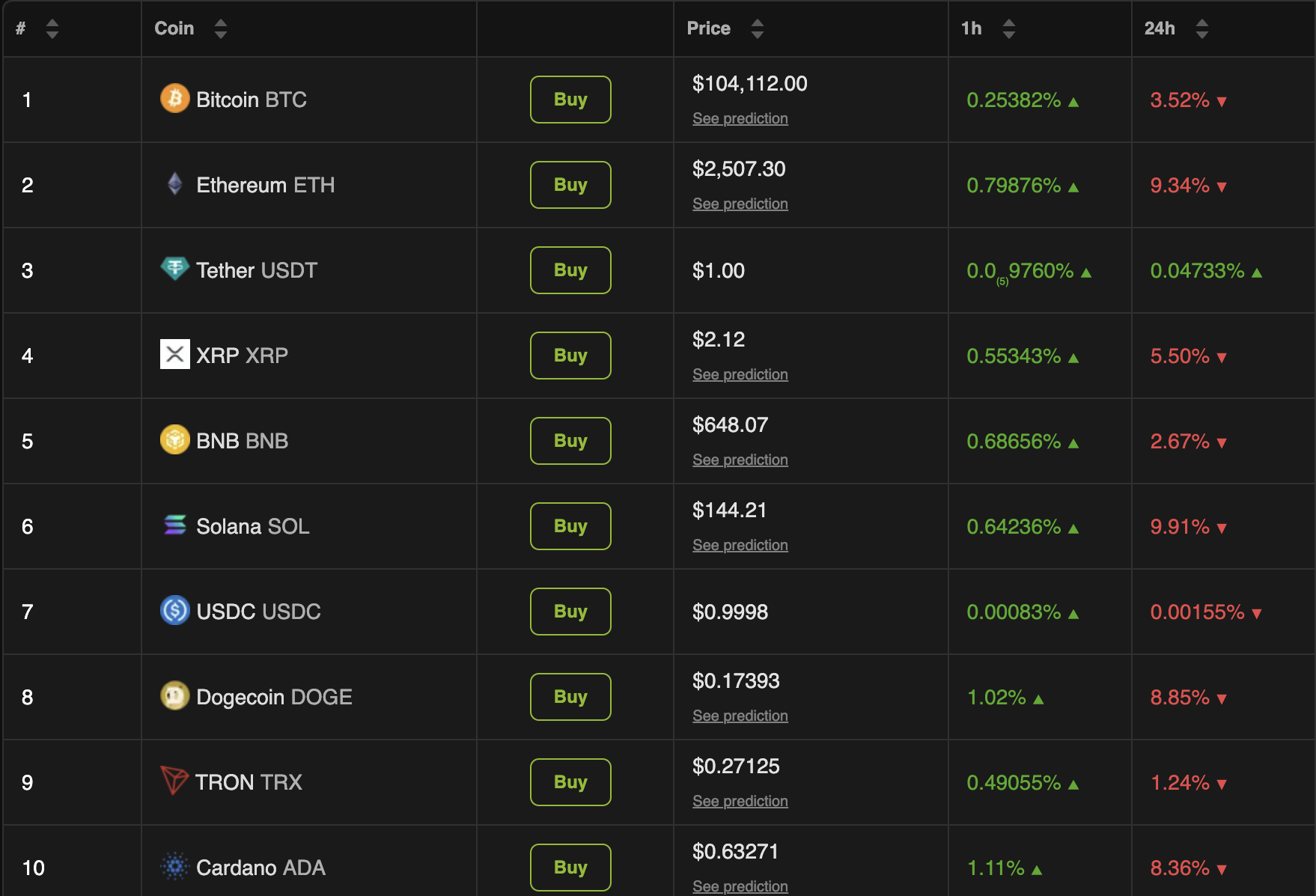

Nine of the top ten coins saw losses over the past day. Bitcoin (BTC) nosedived from over $108,000 to $104,112. However, altcoins suffered the harshest blow.

Crypto Market Cap Post Israel’s Attack On Iran. Source: BeInCrypto

Solana (SOL) lost nearly 10% over the past day. Ethereum (ETH) trailed closely with a 9.3% downtick. Among the top 100 coins, Fartcoin (FARTCOIN) and Ethena (ENA) stood out for double-digit losses of 17.3% and 15.9%, respectively.

These declines forced 247,769 traders out of their positions over the past 24 hours. According to Coinglass data, $1.15 billion has been liquidated from the crypto market.

Bitcoin faced $427.75 million in long and $19.10 million in short liquidations. Ethereum followed with $244.74 million in long liquidations and $43.57 million in short liquidations, highlighting the scale of market turmoil.

Nonetheless, the conflict drove oil and gold up. Oil prices spiked by more than 10%. U.S. West Texas Intermediate rose to $74.99 per barrel, marking a 10.21% uptick.

The global benchmark Brent increased by 10.28% to $76.48 per barrel. Gold also gained 1.2% to reach $3,426.

Analysts Divided Over Israel-Iran Conflict’s Impact on Crypto

As Iran prepares for retaliatory actions, it’s clear that the impact will be felt across markets. Amid this volatility, the cryptocurrency market, particularly Bitcoin, has become a focal point of debate among analysts.

“Bitcoin’s failure to rise against gold—despite over 3.5 years of hype, including a dozen ETFs, Super Bowl ads, El Salvador, NFTs, tens of billions of leveraged buying by MSTR, other Bitcoin treasury companies, the election of a Bitcoin president, and the establishment of a Bitcoin Strategic Reserve—is strong evidence that the bubble has peaked,” Schiff said.

Another analyst echoed his view, claiming that Bitcoin is not a safe haven but more akin to a tech stock.

“It is important to understand that Bitcoin shows its true colors as Israel attacks Iran. It is not an alternative-currency, it is not a safe haven, it is a risk asset, just like another tech stock, that will decline when the market goes to a risk-off posture,” the post read.

However, crypto advocate Anthony Pompliano maintained an optimistic outlook. Drawing parallels to an earlier incident when Iran launched 300 missiles at Israel, Pompliano noted that Bitcoin rebounded to outperform both oil and gold.

“Bitcoin ended up outperforming the other two over the first 48 hours in that situation. Will be interesting to see what happens here,” Pompliano stated.

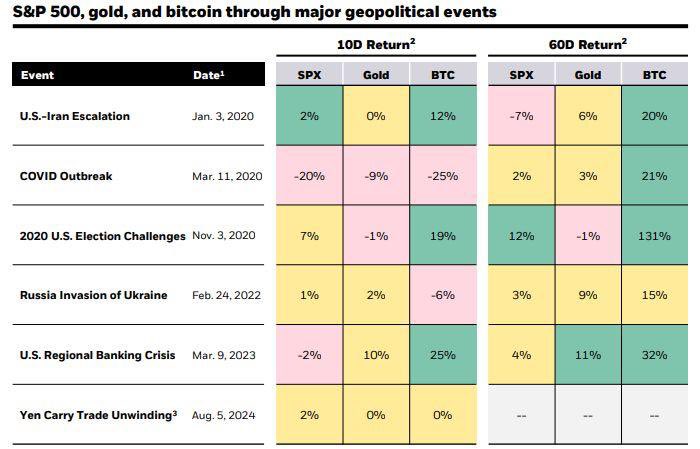

Moreover, a recent BlackRock report revealed that while Bitcoin may underperform in the short term during geopolitical shocks, it has historically rallied double digits within 60 days post-crisis, outpacing gold and equities.

Despite immediate market jitters, this suggests a longer-term bullish outlook for the cryptocurrency. Still, the divide reflects broader uncertainties about Bitcoin’s maturity as an asset, with gold’s millennia-long stability pitted against Bitcoin’s 16-year track record. As markets stabilize, analysts will closely monitor price movements, with some betting on Bitcoin’s recovery and others clinging to gold’s proven reliability.

Fed Chair Jerome Powell is set to testify at Congress today, where the Fed Chair plans to reiterate the Committee’s wait-and-see approach to Fed rate cuts. The Fed Chair is also going to allude to Trump tariffs and warn about how they put the economy at risk of rising inflation. Jerome Powell Reiterates No Hurry

The SEC has yet again cracked down on crypto fraud. The agency has charged the man behind PGI Global, Ramil Palafox, for running a massive $198 million scam through his company, PGI Global, which falsely claimed to be a crypto and forex trading platform.

As per the SEC’s press release, from January 2020 through October 2021, Palafox promised investors massive returns through ‘membership packages’ and also offered them multi-level marketing-like referral incentives in order to encourage them to recruit new investors.

Over $57 Million Investor Funds Misused

Palafox misappropriated over $57 million in investor funds to fund his lavish lifestyle like buying Lamborghinis, items from luxury retailers and for other personal expenses. Further, he also used up the left investor money to pay other investors their returns and referral bonuses, like a classic Ponzi scheme, until it collapsed in 2021.

“As alleged in our complaint, Palafox attracted investors with the allure of guaranteed profits from sophisticated crypto asset and foreign exchange trading, but instead of trading, Palafox bought himself and his family cars, watches, and homes using millions of dollars of investor funds,” said Scott Thompson, Associate Director of the SEC’s Philadelphia Regional Office.

Laura D’Allaird, Chief of the Commission’s new Cyber and Emerging Technologies Unit added that Palafox fooled investors by pretending to be a crypto expert with advanced AI trading technology.

SEC Seeks Penalties and Recovery of Funds

The SEC has charged Palafox with violating anti-fraud and securities laws, seeking permanent bans, the return of ill-gotten gains, and civil penalties. Palafox also faces criminal charges filed by the U.S. Attorney’s Office for the Eastern District of Virginia.

These actions show the SEC’s ongoing efforts to hold individuals and companies accountable for fraudulent activities in the crypto sector. Regulators are increasingly targeting deceptive practices, from Ponzi schemes to illegal staking services, indicating that the crypto space will be held to the same legal standards as traditional financial markets.

The post Crypto News: SEC Exposes Fake Crypto Trading Platform That Cost Investors $198 Million appeared first on Coinpedia Fintech News

The SEC has yet again cracked down on crypto fraud. The agency has charged the man behind PGI Global, Ramil Palafox, for running a massive $198 million scam through his company, PGI Global, which falsely claimed to be a crypto and forex trading platform. As per the SEC’s press release, from January 2020 through October …