The SEC’s Crypto Task Force announced the agenda for its next Roundtable discussion, which will focus on tokenization. The agenda will span two halves, presumably focusing on RWAs and generalized financial instruments.

The Commission announced that this discussion would focus on tokenization in March, but the full agenda provides more complete information. It includes a full list of participants, including many prominent firms.

The SEC Talks Tokenization

Since coming under new leadership this year, the Commission has been hosting Roundtable Discussions on topics in the crypto industry. According to a press release, the SEC’s next talk will concern tokenization, featuring representatives from firms like BlackRock, Nasdaq, Fidelity, Robinhood, Securitize, and more.

“Tokenization is a technological development that could substantially change many aspects of our financial markets. I look forward to hearing ideas from our panelists on how the SEC should approach this area,” Hester “Crypto Mom” Peirce, one of the SEC’s Commissioners, claimed.

Over the last few weeks, the SEC has shown an interest in tokenization. In late April, it planned a regulatory sandbox concerning real estate tokenization with counterparts in El Salvador and private firms. The results of this planning session seemed inconclusive; none of its non-SEC participants are scheduled to appear at the Roundtable. Still, it shows interest.

The discussion is split between two main panels: “Evolution of Finance: Capital Markets 2.0” and “The Future of Tokenization.” Both feature participation from some of the major firms involved, with the US ETF issuers primarily speaking on the first panel.

This could potentially suggest a focus on tokenization as a financial instrument for institutional investors. The latter panel involves RWA advocates like Securitize and Robinhood, possibly indicating that it focuses on RWAs. Still, that’s only speculation.

Other than these general outlines, the SEC hasn’t specified which areas of tokenization are its highest priorities. The Commission first planned this discussion in late March, but today’s agenda is the first major update since then.

Base, a layer-two blockchain developed by Coinbase, has seen a significant surge in Total Value Locked (TVL) over the last 24 hours following a key integration.

It comes amid changing regulatory winds in the US, with President Trump’s pro-crypto stance inspiring bold moves among sector players.

Base TVL Soars 20% As Binance.US Adds Support

According to data on DefiLlama, Base TVL is up by $557 million. It moved from $2.778 billion on Thursday to $3.335 billion as of this writing, a 20% surge in the last 24 hours.

The surge in TVL suggests an increased volume of assets staked, locked, or deposited in the Base blockchain. A higher TVL indicates increased user activity, trust, and adoption, with users committing capital to the protocol.

Meanwhile, this surge follows a notable announcement from Binance.US, the American arm of Binance exchange, the world’s largest crypto trading platform by volume metrics.

According to the announcement, Binance.US now supports Base. It allows Ethereum (ETH) and Circle’s USDC (USD Coin) stablecoin transfers on the Layer-2 network.

“We’re excited to announce that Binance.US now supports Base! Starting today, you can deposit and withdraw Ethereum (ETH) and USDC via Base,” an excerpt in the announcement read.

The exchange highlighted that more assets will join Binance.US on the Base network, indicating interest in developing the integration. Meanwhile, using Base’s blockchain, users can deposit and withdraw ETH and USDC directly to and from Binance.US.

For the exchange, this integration could bolster accessibility. Specifically, Binance.US users can interact with Base’s ecosystem without bridging assets through Ethereum’s mainnet. This is amidst concerns that Ethereum’s mainnet is slow and costly.

As an L2 scaling solution, Base offers faster and lower-cost transactions compared to Ethereum’s mainnet. Data on Etherscan shows Ethereum’s transaction throughput is approximately 13.2 TPS. This could lead to network congestion and high gas fees during peak periods.

On the other hand, Base processes transactions off-chain, bundling them before submitting them to Ethereum. This Method achieves higher throughput and significantly lower fees, making it more cost-effective for users.

Therefore, the integration allows Binance.US users to move ETH and USDC to Base for DeFi activities at a fraction of the cost.

Binance.US suspended its USD deposit and withdrawal services following a high-profile SEC lawsuit and mounting regulatory pressure starting in 2023. However, amid shifted political rhetoric toward crypto, exchanges appear to be taking bold steps.

“Now that we’ve survived, our goal is to help crypto thrive and empower all Americans with freedom of choice,” Binance.US interim CEO Norman Reed said recently.

It aligns with a recent move from the Kraken exchange. As BeInCrypto reported, the US-based exchange listed BNB in a move that marked a strategic shift in US crypto exchanges, potentially signaling broader token adoption in the country.

France responds with new security measures as a string of crypto kidnappings shakes the nation. With three happening in 2025, authorities believe the events are connected.

Interior Minister Bruno Retailleau is working to arrest the perpetrators, protect leading crypto entrepreneurs, and train law enforcement. Still, the father of the most recent victim does not seem satisfied with the measures.

Crypto Kidnapping Wave Strikes France

Typically, crypto thefts take place through hacks and social engineering scams, but that isn’t always the case. In January, a French crypto co-founder was kidnapped in an attempt to steal his private key; he was rescued, but attackers cut a finger off.

Another kidnapping happened in early May, followed by a third attempted this week: a spree is burning through France.

In particular, the details of this last attempted kidnapping shocked the people of France. One woman, the daughter of an exchange’s CEO, was attacked in broad daylight with her partner and 2-year-old child present.

The incident was largely captured on video, further sparking public horror. In response, the authorities have introduced new security measures:

“These repeated kidnappings of professionals in the crypto sector will be fought with specific tools, both immediate and short-term, to prevent, dissuade and hinder in order to protect the industry,” claimed Bruno Retailleau, France’s Interior Minister.

France has enacted a few specific methods to counteract these ambitious kidnapping efforts. Several French crypto leaders have been invited to safety briefings and will receive priority access for emergency calls and regular home visits.

Additionally, law enforcement officers will undergo training on crypto money laundering to better target perpetrators.

Minister Retailleau claimed that several kidnappers have already been arrested. He is also organizing a meeting of France’s prominent crypto entrepreneurs, but the kidnapping victim’s father is unsatisfied.

FRANCE PROMISES SECURITY BOOST FOR CRYPTO ENTREPRENEURS

After a series of violent kidnappings, including attacks on the children of Ledger’s co-founder and Paymium’s CEO, French authorities have announced urgent security measures for the crypto industry.

— Neel (Crypto Jargon) (@Crypto_Jargon) May 16, 2025

Pierre Noziat, CEO of Paymium, told local reporters that he believed this upcoming meeting is only a “communications operation.”

Officials believe these kidnappings are all part of a greater ring, and are taking efforts to track and arrest its members across France.

Hopefully, their investigations will bear fruit. Other countries have also seen aggressive criminals stealing keys and hardware wallets, but a violent conspiracy like this is unprecedented.

According to Johnny Garcia, Managing Director of Institutional Growth and Capital Markets at the VeChain Foundation, Texas will likely become the next state to establish a strategic Bitcoin reserve after New Hampshire.

In an exclusive interview with BeInCrypto, Garcia explained that states with pro-innovation leadership are more inclined to follow New Hampshire’s example. Meanwhile, others may adopt a more cautious, wait-and-see approach.

Why States Like Texas Are More Likely to Follow New Hampshire’s Bitcoin Reserve Lead

The VeChain executive described New Hampshire’s passage of House Bill 302 as a ‘landmark moment’ for digital assets. He stated that the development highlights Bitcoin’s growing recognition as a strategic financial instrument.

It also lays the groundwork to encourage wider blockchain adoption by normalizing digital assets in public portfolios.

“Momentum has been gathering at the State level since the presidential inauguration, and have commented before, there is a sea change taking place in the minds of State representatives across the general perception of Bitcoin [and other crypto assets] in the US,” Garcia told BeInCrypto.

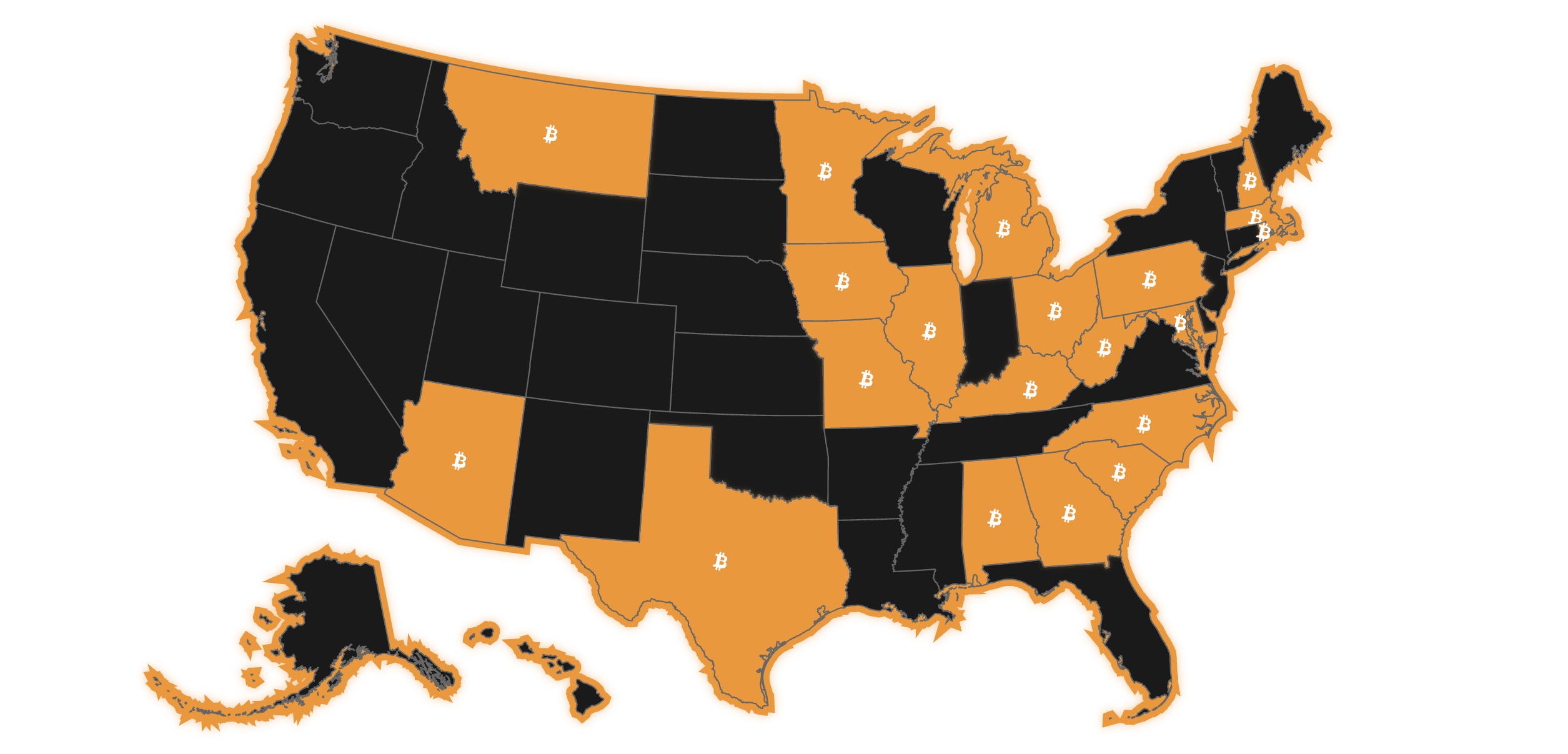

Importantly, he believes the move could prompt the states already considering related legislation to accelerate their efforts so they don’t fall behind. The latest data from Bitcoin Laws shows that as of May 2025, 37 digital asset-related bills are active in 20 states.

Live Bitcoin Reserve Bills Across 20 States. Source: Bitcoin Laws

However, Garcia emphasized that the success of these bills depends on various factors. These include a state’s political climate, economic priorities, and risk tolerance.

“States with pro-innovation leadership, like Texas or Utah, are more likely to follow New Hampshire’s lead in short order, while others may wait to see how things play out for N.H,” he added.

With Texas now in the spotlight, there is strong optimism that similar legislation will be signed into law. Republican Governor Greg Abbott has expressed a favorable outlook toward the industry. The Texas Legislative session ends on June 2, so the decision could come any day now.

This trend highlights a clear difference of opinion between Democrats and Republicans regarding investments in digital asset reserves, a divide Garcia also acknowledges.

“These differences are nothing new, and I chalk them up to deeper-rooted perspectives, just like there are conservatives and liberals, or risk takers and those who like to play things safe. Some may try to tease out those groups and label people on one side as Democratic and the other as Republican, but I think that is too simplistic,” he said.

He acknowledged that bridging this gap poses a significant, but surmountable, challenge. The executive noted that increased cooperation can be fostered through education and a deeper understanding of the technology’s potential benefits and risks.

According to Garcia, the focus should be on identifying shared goals, such as leveraging blockchain to improve efficiency and transparency in government operations—an approach that could lay the groundwork for bipartisan collaboration.

“The ultimate goal would be to develop a thoughtful and balanced approach to digital assets that can benefit all Americans, regardless of political affiliation. This can be achieved by moving the conversation beyond partisan lines and focusing on the long-term economic and technological implications,” Garcia disclosed to BeInCrypto.

How Will State-Level Interest Impact Broader Crypto Adoption?

Whether Democrats and Republicans will ever fully agree on digital assets remains uncertain. Despite this, the introduction of bills and increased discussions at the state level signal growing interest and momentum.

Garcia said this shift marks a fundamental change in how public finance views blockchain assets, recognizing them as tools for innovation and resilience.

“It, combined with the strength of Bitcoin, has rekindled the discussion around ‘digital gold’ and could help reshape public finance by introducing decentralized, censorship-resistant assets into traditional portfolios,” he commented.

It normalizes digital assets as a strategic asset class, not just speculative. This encourages more institutional and enterprise participation.

This also pushes policymakers and the public to better understand digital assets’ risks and benefits, which can lead to clearer and better regulations.

It helps build infrastructure like regulated custody and on-chain auditability. This makes blockchain adoption easier for businesses.

He also said that while accessibility remains a challenge for mainstream adoption, state-backed initiatives could foster partnerships between the public and private sectors. This collaboration could lead to the development of user-friendly wallets, custody services, and decentralized finance platforms, expanding access for both retail and institutional users.

“This aligns with our focus at VeChain on scalable, enterprise-grade blockchain solutions, and we anticipate that state-level adoption will create a ripple effect, accelerating the integration of digital assets into both public and private sectors,” Garcia remarked.

The Balance Between Opportunity and Risk in State Crypto Holdings

While the benefits inspire optimism, the reserves carry several implications for a common taxpayer. Garcia explained that supporters believe state investments could boost long-term returns and diversify away from inflation-prone assets, potentially strengthening the state’s finances and benefiting taxpayers. Yet, he claimed,

“We have not yet reached the point where Bitcoin has achieved a greater level of stability, and if it sees a similar pullback compared to previous cycles, that would greatly diminish interest in setting up reserves and could cost taxpayers money.”

Garcia warned that significant price drops could lead to losses in the state’s reserves. Thus, if the allocation is too large or poorly managed, this could potentially threaten financial stability.

“This could, in theory, lead to pressure for tax policy changes to offset those losses, although this would depend heavily on the scale of the investment and the state’s overall financial health,” he mentioned to BeInCrypto.

Garcia advocated educating taxpayers about both the benefits and risks to maintain public trust. He emphasized that the long-term impact will depend on the responsible and strategic management of these reserves.

Beyond tax concerns, Garcia detailed several challenges states may face when implementing crypto reserves.

“The volatility of digital assets remains the biggest challenge facing states looking to implement reserves, as managing this volatility within a public treasury framework will require careful consideration and potentially sophisticated risk management strategies,” he commented.

Garcia also mentioned that educating lawmakers and the public is crucial for wider acceptance, as many state officials lack expertise in digital asset management and will need training or specialists. He underlined that federal regulatory uncertainty adds complexity. Therefore, clear rules on custody and reporting are necessary.

According to Garcia, transparency and strong cybersecurity measures are other key factors essential to ensuring the long-term success of these initiatives.

The Road to a National Strategic Bitcoin Reserve

Meanwhile, Garcia pointed out that concerns over taxes and market volatility are why President Trump’s Bitcoin reserve does not include provisions for investing the country’s funds. Instead, it focuses on using forfeited assets to build the stockpile.

The SBR would involve acquiring 1 million Bitcoins over five years and holding them for at least 20 years. Garcia declared that allowing direct Bitcoin investments would depend on shifting political and economic factors.

“Allowing for such purchases will require bipartisan support in both the House and the Senate, along with the President’s signature, but as the recent stall for the GENIUS Act shows, lawmakers are far from being on the same page,” the executive shared with BeInCrypto.

Garcia believes that a clear regulatory framework for crypto and a plan to incorporate Bitcoin into a strategic reserve will eventually be established by law. Nonetheless, the timeline and specific details of these bills remain ‘challenging to predict.’

FRANCE PROMISES SECURITY BOOST FOR CRYPTO ENTREPRENEURS

FRANCE PROMISES SECURITY BOOST FOR CRYPTO ENTREPRENEURS