A disturbing new scam is leveraging the obscure OP_RETURN feature in Bitcoin transactions to target one of the most infamous addresses in crypto history — the 1Feex wallet containing approximately 80,000 BTC stolen from Mt. Gox.

That stash is worth over $8.7 billion at current prices, making it a prime target for fraudsters attempting to claim legal rights over it.

How OP_RETURN Is Helping Scammers Target Mt. Gox’s Missing 80,000 Bitcoin

The Mt. Gox collapse in 2014 resulted in 850,000 BTC going missing. Although 140,000 BTC were recovered for creditor repayments, wallets like 1Feex have remained untouched until now.

Whoever is behind the scam is likely banking on two outcomes. The first is collecting sensitive user data by masquerading as the wallet’s custodian.

Second, they are laying the groundwork for a legal claim to ownership, perhaps similar to past lawsuits aimed at forcing Bitcoin developers to hand over access to lost coins.

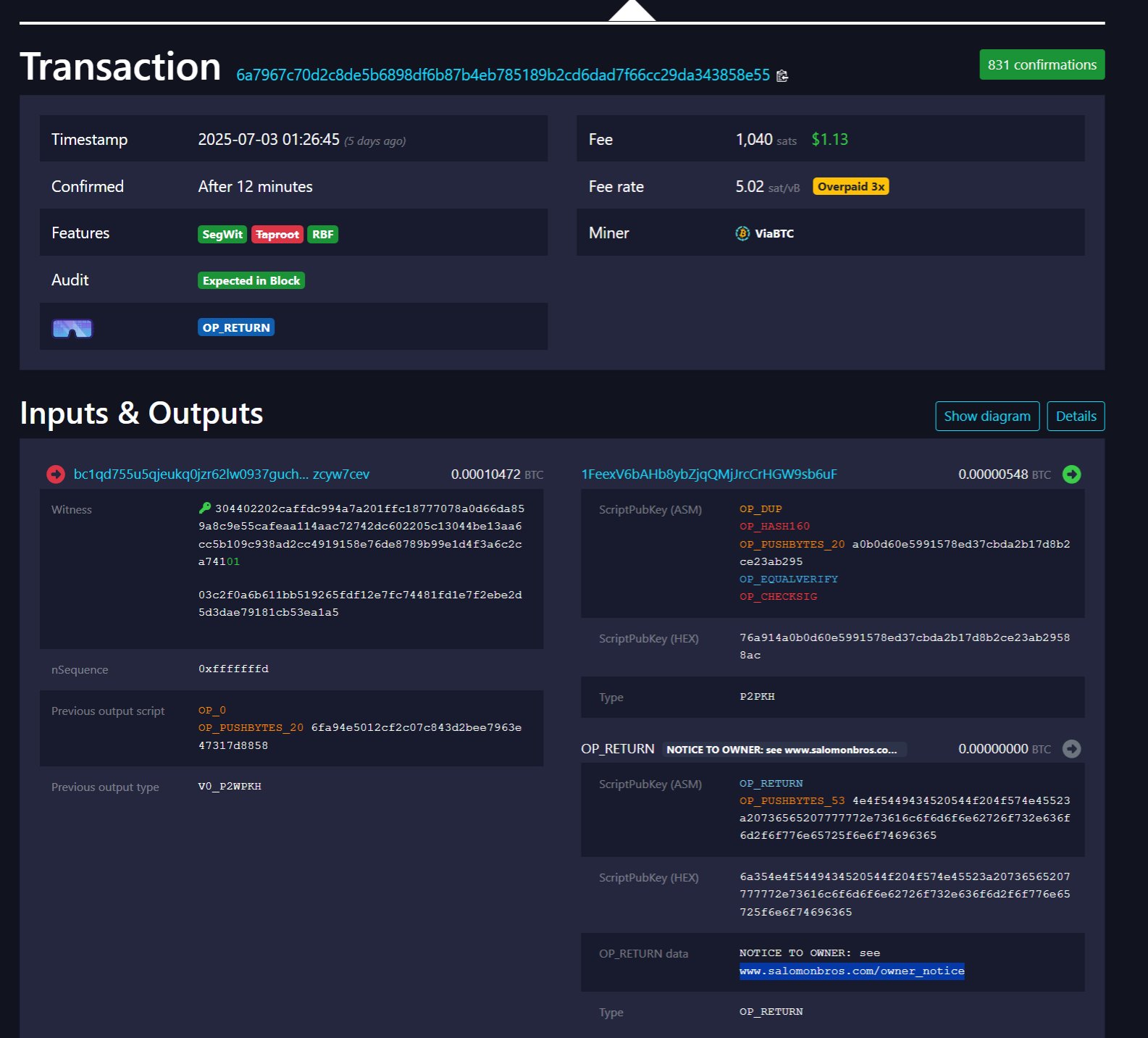

Going by the latter, BitMEX Research has uncovered a scam. It involves sending small transactions to legacy Bitcoin addresses using the OP_RETURN field. This is a space in the Bitcoin blockchain meant to store arbitrary data.

One such transaction to the dormant 1Feex address contains a message directing viewers to a suspicious website.

“NOTICE TO OWNER: see www.salomon[]bros.[]com/owner_notice,” BitMEX Research revealed.

The linked website represents a client who has taken “constructive possession” of the wallet and is seeking to identify a “bona fide owner.”

— matthew sigel, recovering CFA (@matthew_sigel) July 8, 2025

Matthew Sigel, Head of Digital Assets Research at VanEck, reflects broader concerns in the crypto community, especially regarding the scam’s legal framing.

Why Calvin Ayre’s Legal History Resurfaces in OP_RETURN Ownership Controversy

Users immediately mentioned Calvin Ayre, a longtime Bitcoin SV proponent and controversial figure. Ayre has reportedly funded legal actions asserting ownership over dormant or stolen Bitcoin.

Calvin funded a case where ownership of this exact address was claimed. Legal action was taken against the Bitcoin developers over it

However, some users took this insight with a pinch of salt, cautioning against slander. More closely, one user asked for proof that Ayre has run phishing-style scams.

I’m not following. So there is a shady website listed in the op return that could collect personal information?

Why would somebody who moves 80k coins participate in such a scam? There is a short list of people this could be?

Notwithstanding, the fact remains that OP_RETURN is now being weaponized in a gray zone between spam and pseudo-legal attacks.

Meanwhile, this scam arrives amid renewed controversy over OP_RETURN limits in Bitcoin Core. BeInCrypto reported on a proposal to restrict OP_RETURN data to 80 bytes under Bitcoin Core v0.30. The report cites network bloat and spam concerns.

While the limit remains under review, the new wave of scams may give fresh weight to the argument for tighter controls.

“OP_RETURN outputs greater than 83 bytes will increase significantly, UTXO bloat will keep getting worse and there will be more garbage on chain. This is going to age like a bad tattoo,” self-proclaimed Bitcoin expert Jimmy Song said at the time.

Further, in late April, BeInCrypto reported a rift among Bitcoin Core developers triggered by Peter Todd’s proposal to restrict OP_RETURN even further.

Critics argued that it would stifle innovation and off-chain use cases. Meanwhile, others supported it to reduce attack surfaces and abuse.

Also, Bitcoin should not follow an “L2 centric” roadmap. It’s actually what killed Ethereum.

However, as this new exploit demonstrates, OP_RETURN is now being twisted for phishing schemes. Bad actors prey on legal uncertainty and dormant assets.

In this case, billions are at stake as the line between technical freedom and exploitable vectors is again under scrutiny. The interest comes as OP_RETURN transactions anchor these messages immutably into Bitcoin’s ledger.

The metrics used to measure outcomes can be misleading when evaluating blockchain performance. As more blockchain networks emerge, the public needs clear, efficiency-focused metrics, rather than exaggerated claims, to differentiate between them.

In a conversation with BeInCrypto, Taraxa Co-Founder Steven Pu explained that it’s becoming increasingly difficult to compare blockchain performance accurately because many reported metrics rely on overly optimistic assumptions rather than evidence-based results. To combat this wave of misrepresentation, Pu proposes a new metric, which he calls TPS/$.

Why Does the Industry Lack Reliable Benchmarks?

The need for clear differentiation is growing with the increasing number of Layer-1 blockchain networks. As various developers promote the speed and efficiency of their blockchains, relying on metrics that distinguish their performance becomes indispensable.

However, the industry still lacks reliable benchmarks for real-world efficiency, instead relying on sporadic sentimental waves of hype-driven popularity. According to Pu, misleading performance figures currently saturate the market, obscuring true capabilities.

“It’s easy for opportunists to take advantage by driving up over-simplified and exaggerated narratives to profit themselves. Every single conceivable technical concept and metric has at one time or another been used to hype up many projects that don’t really deserve them: TPS, finality latency, modularity, network node count, execution speed, parallelization, bandwidth utilization, EVM-compatibility, EVM-incompatibility, etc.,” Pu told BeInCrypto.

Pu focused on how some projects exploit TPS metrics, using them as marketing tactics to make blockchain performance sound more appealing than it might be under real-world conditions.

Examining the Misleading Nature of TPS

Transactions per second, more commonly known as TPS, is a metric that refers to the average or sustained number of transactions that a blockchain network can process and finalize per second under normal operating conditions.

However, it often misleadingly hypes projects, offering a skewed view of overall performance.

“Decentralized networks are complex systems that need to be considered as a whole, and in the context of their use cases. But the market has this horrible habit of over-simplifying and over-selling one specific metric or aspect of a project, while ignoring the whole. Perhaps a highly centralized, high-TPS network does have its uses in the right scenarios with specific trust models, but the market really has no appetite for such nuanced descriptions,” Pu explained.

Pu indicates that blockchain projects with extreme claims on single metrics like TPS may have compromised decentralization, security, and accuracy.

“Take TPS, for example. This one metric masks numerous other aspects of the network, for example, how was the TPS achieved? What was sacrificed in the process? If I have 1 node, running a WASM JIT VM, call that a network, that gets you a few hundred thousand TPS right off the bat. I then make 1000 copies of that machine and call it sharding, now you start to get into the hundreds of millions of ‘TPS’. Add in unrealistic assumptions such as non-conflict, and you assume you can parallelize all transactions, then you can get “TPS” into the billions. It’s not that TPS is a bad metric, you just can’t look at any metric in isolation because there’s so much hidden information behind the numbers,” he added.

The Taraxa Co-founder revealed the extent of these inflated metrics in a recent report.

The Significant Discrepancy Between Theoretical and Real-World TPS

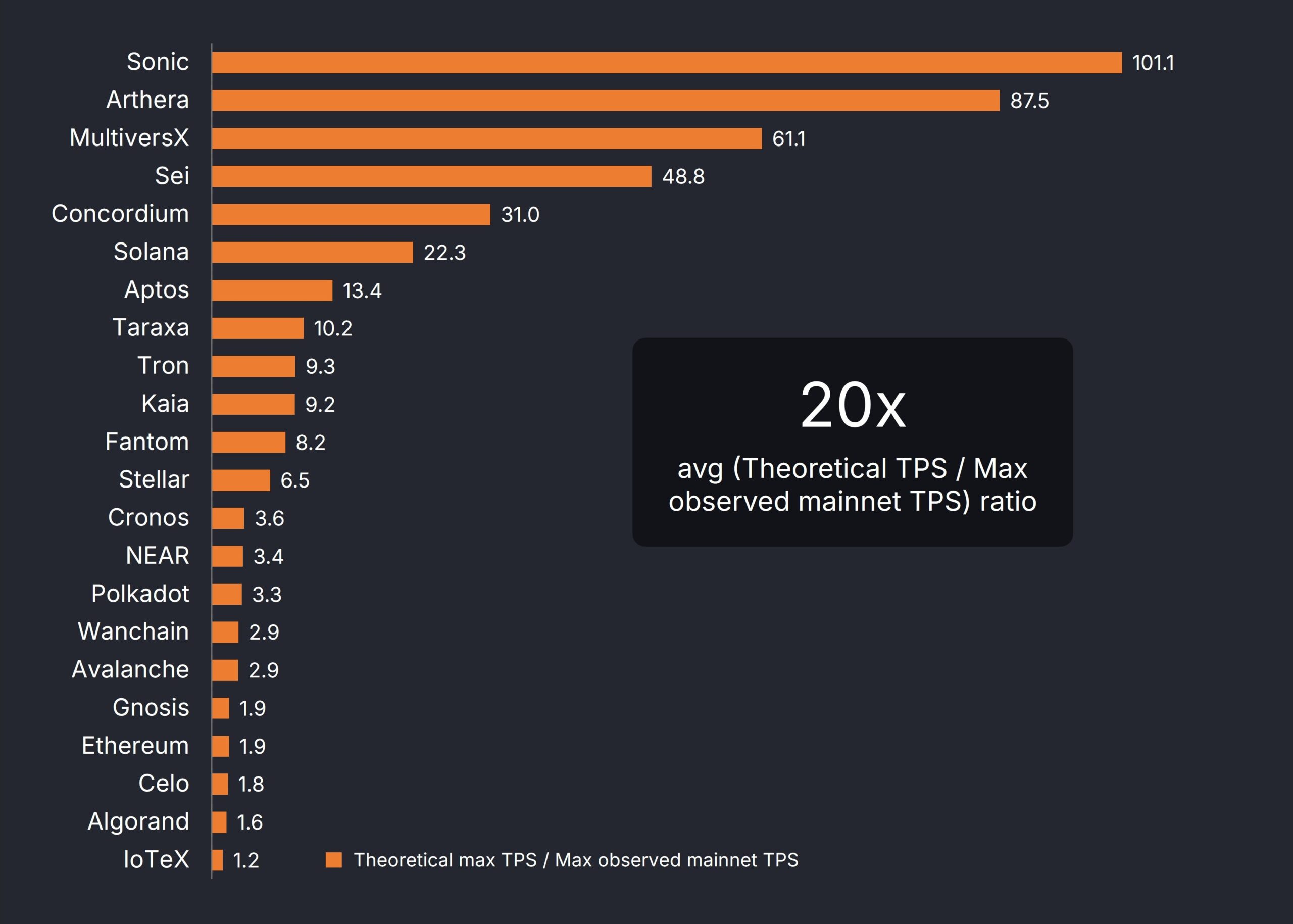

Pu sought to prove his point by determining the difference between the maximum historical TPS realized on a blockchain’s mainnet and the maximum theoretical TPS.

Of the 22 permissionless and single-shard networks observed, Pu found that, on average, there was a 20-fold gap between theory and reality. In other words, the theoretical metric was 20 times higher than the maximum observed mainnet TPS.

Taraxa Co-founder finds 20x difference between the Theoretical TPS and the Max Observed Mainnet TPS. Source: Taraxa.

“Metric overestimations (such as in the case of TPS) are a response to the highly speculative and narrative-driven crypto market. Everyone wants to position their project and technologies in the best possible light, so they come up with theoretical estimates, or conduct tests with wildly unrealistic assumptions, to arrive at inflated metrics. It’s dishonest advertising. Nothing more, nothing less,” Pu told BeInCrypto.

Looking to counter these exaggerated metrics, Pu developed his own performance measure.

Introducing TPS/$: A More Balanced Metric?

Pu and his team developed the following: TPS realized on mainnet / monthly $ cost of a single validator node, or TPS/$ for short, to fulfill the need for better performance metrics.

This metric assesses performance based on verifiable TPS achieved on a network’s live mainnet while also considering hardware efficiency.

The significant 20-fold gap between theoretical and actual throughput convinced Pu to exclude metrics based solely on assumptions or lab conditions. He also aimed to illustrate how some blockchain projects inflate performance metrics by relying on costly infrastructure.

“Published network performance claims are often inflated by extremely expensive hardware. This is especially true for networks with highly centralized consensus mechanisms, where the throughput bottleneck shifts away from networking latency and into single-machine hardware performance. Requiring extremely expensive hardware for validators not only betrays a centralized consensus algorithm and inefficient engineering, it also prevents the vast majority of the world from potentially participating in consensus by pricing them out,” Pu explained.

Pu’s team located each network’s minimum validator hardware requirements to determine the cost per validator node. They later estimated their monthly cost, paying particular attention to their relative sizing when used to compute the TPS per dollar ratios.

“So the TPS/$ metric tries to correct two of the perhaps most egregious categories of misinformation, by forcing the TPS performance to be on mainnet, and revealing the inherent tradeoffs of extremely expensive hardware,” Pu added.

Pu stressed considering two simple, identifiable characteristics: whether a network is permissionless and single-sharded.

Permissioned vs. Permissionless Networks: Which Fosters Decentralization?

A blockchain’s degree of security can be unveiled by whether it operates under a permissioned or permissionless network.

Permissioned blockchains refer to closed networks where access and participation are restricted to a predefined group of users, requiring permission from a central authority or trusted group to join. In permissionless blockchains, anyone is allowed to participate.

According to Pu, the former model is at odds with the philosophy of decentralization.

“A permissioned network, where network validation membership is controlled by a single entity, or if there is just a single entity (every Layer-2s), is another excellent metric. This tells you whether or not the network is indeed decentralized. A hallmark of decentralization is its ability to bridge trust gaps. Take decentralization away, then the network is nothing more than a cloud service,” Pu told BeInCrypto.

Attention to these metrics will prove vital over time, as networks with centralized authorities tend to be more vulnerable to certain weaknesses.

“In the long term, what we really need is a battery of standardized attack vectors for L1 infrastructure that can help to reveal weaknesses and tradeoffs for any given architectural design. Much of the problems in today’s mainstream L1 are that they make unreasonable sacrifices in security and decentralization. These characteristics are invisible and extremely hard to observe, until a disaster strikes. My hope is that as the industry matures, such a battery of tests will begin to organically emerge into an industry-wide standard,” Pu added.

Meanwhile, understanding whether a network employs state-sharding versus maintaining a single, sharded state reveals how unified its data management is.

State-Sharding vs. Single-State: Understanding Data Unity

In blockchain performance, latency refers to the time delay between submitting a transaction to the network, confirming it, and including it in a block on the blockchain. It measures how long it takes for a transaction to be processed and become a permanent part of the distributed ledger.

Identifying whether a network employs state-sharding or a single-sharded state can reveal much about its latency efficiency.

State-sharded networks divide the blockchain’s data into multiple independent parts called shards. Each shard operates somewhat independently and doesn’t have direct, real-time access to the complete state of the entire network.

By contrast, a non-state-sharded network has a single, shared state across the entire network. All nodes can access and process the same complete data set in this case.

Pu noted that state-sharded networks aim to increase storage and transaction capacity. However, they often face longer finality latencies due to a need to process transactions across multiple independent shards.

He added that many projects adopting a sharding approach inflate throughput by simply replicating their network rather than building a truly integrated and scalable architecture.

“A state-sharded network that doesn’t share state, is simply making unconnected copies of a network. If I take a L1 network and just make 1000 copies of it running independently, it’s clearly dishonest to claim that I can add up all the throughput across the copies together and represent it as a single network. There are architectures that actually synchronize the states as well as shuffle the validators across shards, but more often than not, projects making outlandish claims on throughput are just making independent copies,” Pu said.

Based on his research into the efficiency of blockchain metrics, Pu highlighted the need for fundamental shifts in how projects are evaluated, funded, and ultimately succeed.

What Fundamental Shifts Does Blockchain Evaluation Need?

Pu’s insights present a notable alternative in a Layer-1 blockchain space where misleading performance metrics increasingly compete for attention. Reliable and effective benchmarks are essential to counter these false representations.

“You only know what you can measure, and right now in crypto, the numbers look more like hype-narratives than objective measurements. Having standardized, transparent measurements allows simple comparisons across product options so developers and users understand what it is they’re using, and what tradeoffs they’re making. This is a hallmark of any mature industry, and we still have a long way to go in crypto,” Pu concluded.

Adopting standardized and transparent benchmarks will foster informed decision-making and drive genuine progress beyond merely promotional claims as the industry matures.

Since April 23, Solana’s price has oscillated within a tight trading range, facing resistance near $153.67 and finding support around $145.68.

A growing wave of bearish pressure threatens to break this range to the downside, with a key technical indicator on the verge of confirming a major sell signal.

Solana Faces Breakdown Risk as Sellers Tighten Grip

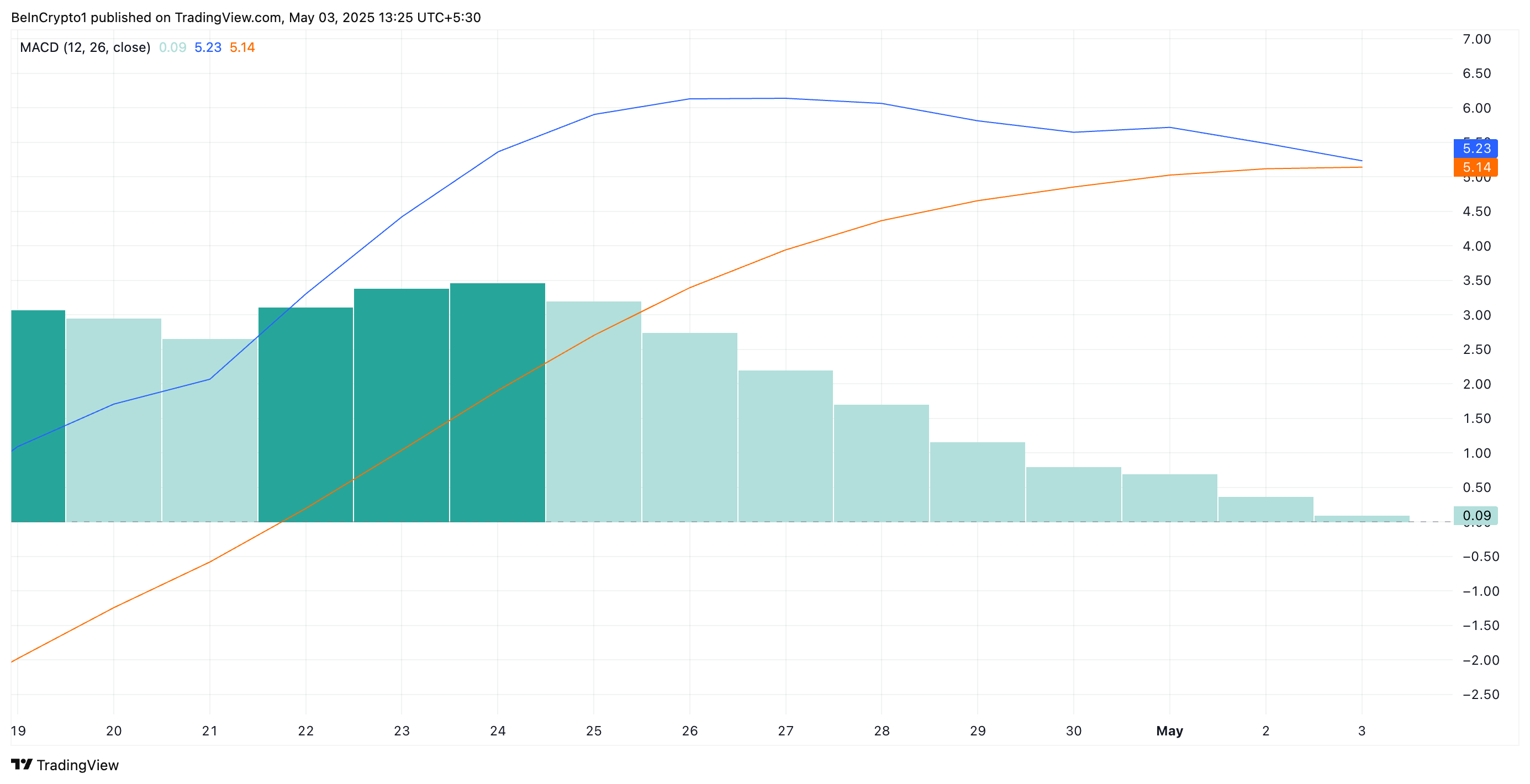

SOL’s Moving Average Convergence Divergence (MACD) indicator is poised to form a death cross, a bearish crossover where the MACD line dips below the signal line.

As of this writing, the coin’s MACD line (blue) rests near the signal line (orange), awaiting a catalyst to push it under. This pattern often precedes a sustained downtrend and is widely viewed by traders as a sign of weakening price strength.

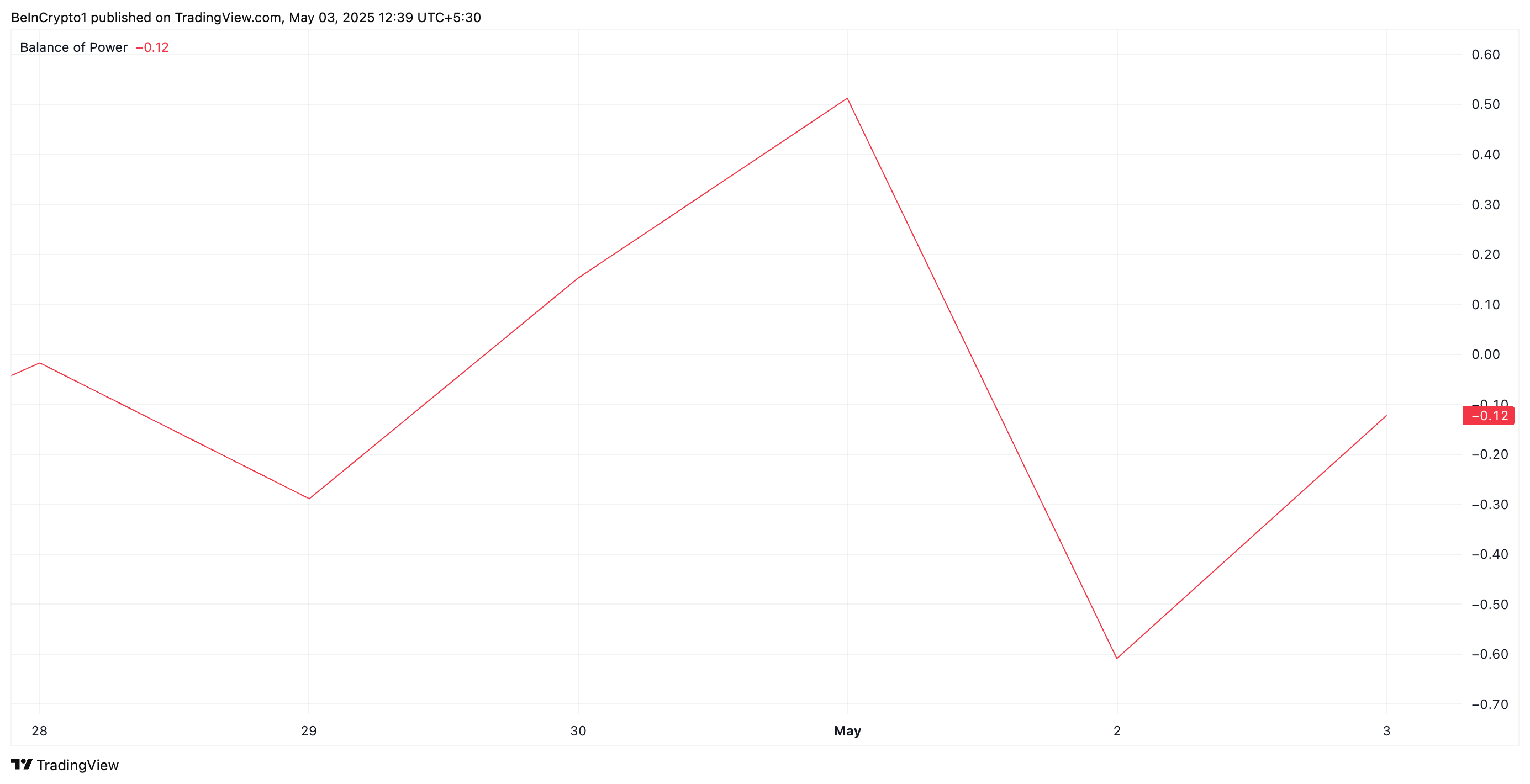

Further, SOL’s Balance of Power (BoP) is currently negative, reinforcing the downtrend. This indicates that sellers have gained market control. At press time, this stands at -0.12.

The BoP indicator measures the strength of buying versus selling pressure by comparing the closing price to the trading range over a given period.

When an asset’s BoP is positive, it signals that buyers are in control, indicating strong upward momentum and potential for continued price gain.

On the other hand, as with SOL, a negative BoP value indicates that sellers dominate the market. It suggests an increase in downward pressure on SOL and hints at the potential commencement of a new decline phase.

SOL Faces Key Support Test Amid Mounting Sell Pressure

As bearish momentum builds, SOL risks breaking below the support level at $145.68. A decisive break beneath this threshold would confirm a short-term downtrend and potentially trigger a deeper decline toward $142.32.

Should buyers fail to regain control at that point, SOL could slide further to test the lower support at $133.94.

However, this bearish outlook could be invalidated if fresh demand emerges and buying interest strengthens. In that bullish scenario, SOL may overcome resistance at $153.67, opening the door for a rally toward $171.50.

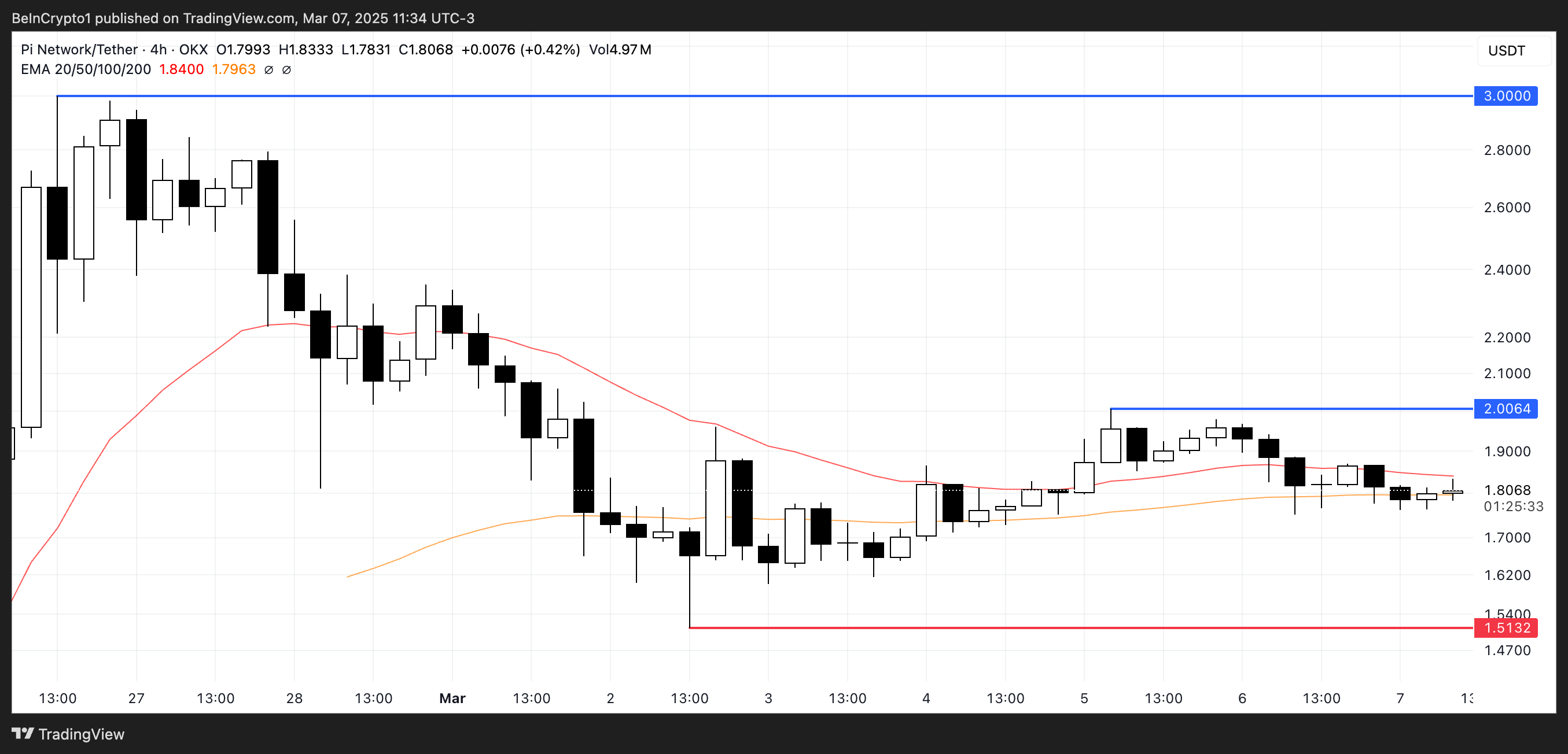

Pi Network (PI) has been consolidating after hitting new highs in late February, with technical indicators showing mixed signals. The DMI chart suggests that sellers are attempting to maintain control, as the +DI has dropped while the -DI is rising, signaling increasing bearish momentum.

Meanwhile, the RSI remains neutral, fluctuating between 45 and 55, indicating a lack of strong directional movement. If a strong uptrend emerges, PI could break above $2 and potentially test $3, but downside risks remain, especially with the upcoming unlock of 188 million tokens this month.

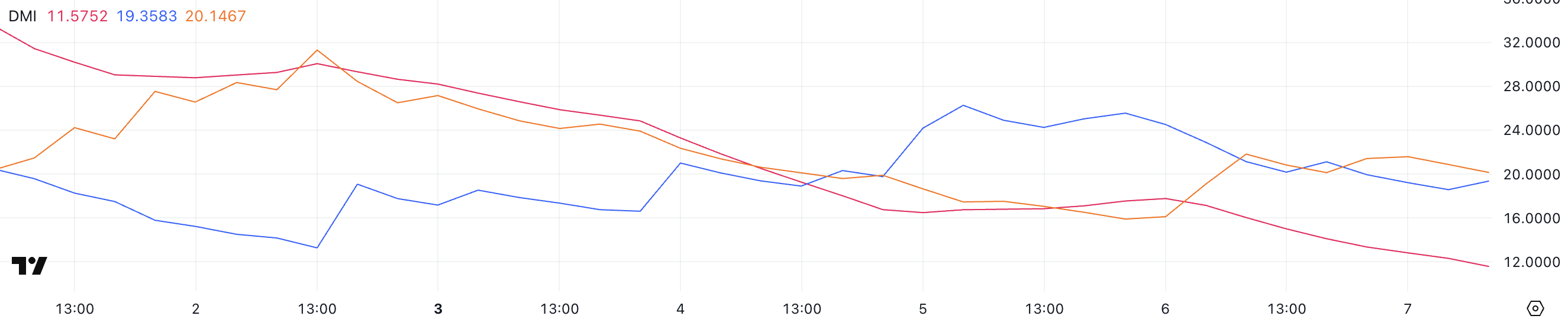

Pi Network DMI Shows Sellers Are Trying To Keep Control

Pi Network’s DMI chart shows that its ADX has dropped to 11.5, down from 17.7 the previous day.

The Average Directional Index (ADX) measures trend strength on a scale from 0 to 100, with values below 20 indicating a weak trend and readings above 25 suggesting a strong trend.

A declining ADX suggests that the current trend, whether bullish or bearish, is losing momentum and is less likely to continue in the short term.

At the same time, PI +DI has fallen to 19.3 from 24.5, while -DI has risen to 20.1 from 16.1. This shift indicates that bearish momentum is increasing as selling pressure overtakes buying pressure.

For a bullish reversal, +DI would need to reclaim dominance over -DI alongside an ADX increase, confirming a stronger trend direction.

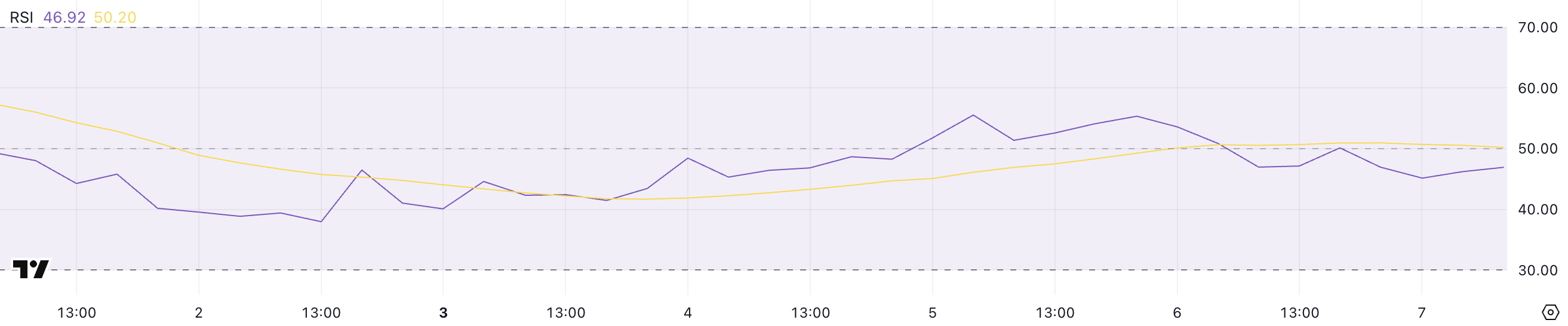

PI RSI Has Been Neutral For 8 Days

Pi Network’s RSI is currently at 46.9, maintaining a neutral stance since February 27 and fluctuating between 45 and 55 for the past three days.

The Relative Strength Index (RSI) is a momentum indicator that measures the speed and magnitude of price movements on a scale from 0 to 100.

Readings above 70 indicate overbought conditions, suggesting a potential pullback, while readings below 30 signal oversold conditions, hinting at a possible rebound. A neutral RSI between 45 and 55 typically reflects a lack of strong momentum in either direction.

With PI RSI sitting at 46.9, the market appears indecisive, lacking clear bullish or bearish momentum. This suggests that Pi Network’s price may remain range-bound unless a significant shift in buying or selling pressure occurs.

For a stronger bullish outlook, the RSI would need to break above 55, signaling increasing buying interest, while a drop below 45 could indicate growing bearish momentum, potentially leading to further price declines.

Consolidation periods often indicate a temporary pause in price movement as traders assess the next direction, with the potential for either a continuation of the previous trend or a reversal.

If buying pressure returns and Pi Network resumes its uptrend, it could first test resistance around $2. A breakout above this level, combined with strong momentum, could push Pi toward $3 and even higher, marking new all-time highs.

However, if the uptrend fails to materialize and selling pressure increases, PI price could enter a corrective phase. In this scenario, the price could decline toward $1.51. Its next price movements could be driven by its 188 million token unlock, which will take place this month.

(@alipaints) April 29, 2025