Robinhood has introduced staking for Ethereum (ETH) and Solana (SOL) to its U.S. customers, enabling them to earn rewards by locking their crypto assets on the platform. The feature requires a minimal stake, making it accessible for a wide range of investors. This launch broadens Robinhood’s crypto services amid growing demand for passive income opportunities in decentralized finance. The move positions Robinhood to compete more aggressively in the expanding crypto market.

XRP price managed to retake the $2.3 level on Wednesday US SEC decision to delay altcoin spot ETF decision triggered an initial pullback towards $2.24. Can Ripple CEO, Brad Garlinhouse’ latest product proposal spur more gains in the days ahead?

XRP has maintained its footing above the $2.00 mark this week, even as the U.S. Securities and Exchange Commission (SEC) postponed its decision on multiple altcoin ETFs.

Ripple (XRP) Price Action| Source: Coingecko

On Tuesday, April 29, Ripple price is floating between $2.01 and $2.17, reflecting a 4.2% gain over the past seven days, signalling that the intially sell-off after the SEC announced the delayed verdict.

The delay in ETF decisions, particularly affecting Solana, Cardano, and Avalanche, and XRP. This intitaily caused a capital rotation back into BTC and ETH, as XRP price plunged to a daily timeframe low of $2.3

However, Bloomberg analyst Eric Balchunas confirmed that the delay were part of normal review procedure of the SEC, reitarating high chances of approval. Following this, altcoin markets regained balances, with XRP price risking 1.7% to retake the $2.30 level at press time.

Ripple Founder Salary Proposal Inspires Payment Model Shift

Ripple CEO Brad Garlinghouse has reignited conversation around blockchain’s XRP’s real-world use cases. An X post shared by prominent analyst “CryptoSensei” showed Brad Garlinghouse proposing a new Salary model for workers globally.

“Why not get paid daily, hourly, or even by the second? – Garlinghouse asked.

The idea centers on eliminating outdated friction in global payments. Garlinghouse argued that the current monthly or biweekly paycheck system exists only due to settlement lag in traditional finance. In contrast, Ripple’s on-chain payments infrastructure could enable seamless, real-time compensation flows.

With RippleNet and the XRP Ledger already enabling low-cost, cross-border payments, analysts believe Garlinghouse’s idea could become a core use case for XRP. Enabling Real-time salary estimation and micro-payments would position XRP more major gains and international adoption.

This proposal may have contributed to XRP’s intraday price recovery above the $2.30 level at the time of publication on Wednesday.

XRP Price Forecast: Can Ripple Founder’s Proposal Drive XRP Price to $5?

The $5 XRP price target is gaining traction once again, as both technical patterns and market narrative momentum align for a mild rebound above $2.30 on Wednesday.

Garlinghouse’s salary streaming proposal could ignite interest among fintech leaders and institutional players exploring payroll automation. If Ripple successfully launches real-world applications of micro-wage payments via XRP, the coin could instantly evolve from a speculative asset into a core financial utility.

Short-Term XRP Technical Outlook: Momentum Builds but Resistance Looms at $3.50

XRP is currently trading at $2.2499, having posted a marginal daily gain of +0.53%. The asset is trading just below the Keltner Channel midline resistance of $2.3877, a level that will likely serve as the first major hurdle for bullish continuation.

The Relative Strength Index on Moving Average (RSIOMA) shows bullish convergence:

RSI is currently at 68.87, approaching the overbought zone.

The RSI MA has trended higher to 54.55, supporting ongoing momentum.

A bullish crossover occurred mid-April, and the green histogram continues to widen, suggesting sustained buyer interest. However, volume has yet to show explosive growth, with daily trading volumes capped at 18.58M, indicating the current rally is still fragile without stronger accumulation support.

Key Technical Levels:

Support: $2.17 (Keltner mid-band), followed by $1.96

Resistance: $2.39 (Keltner upper band), and psychological threshold at $2.50

RSI Critical Zone: A break above 70 could accelerate buying pressure

XRP Price Forecast

If Ripple executes its payroll automation vision using XRP as a settlement token, market perception could shift dramatically.

Utility-driven narratives are likely to attract institutional flows, particularly if the model demonstrates cost savings and scalability across borders.

In such a scenario, technical targets beyond $3.50 toward the $5 mark become realistic over the next 6–12 months—conditional on:

Regulatory clarity in the U.S. and Europe

Stablecoin legislations in progress and sustained partnerships with enterprise clients

Continued growth in on-chain settlement volume

Conclusion

While XRP’s breakout toward $5 remains speculative in the short term, both technical momentum and growing utility narratives offer a compelling setup. A breakout above $2.39 with volume confirmation could mark the next leg up.

Dogecoin has been among the top-traded tokens, which has been attracting enough liquidity, which has maintained the volatility. Meanwhile, the latest price action has remained stuck within a narrow range, hinting towards a drop in the bullish and bearish pressures. While the spot market remains uncertain, the whales seem to be confident of the upcoming price action as they continue to transfer huge amounts of DOGE but without impacting the DOGE price rally.

As per the data from a popular reporting platform, Whale Alert, an interesting transfer of over 478 million DOGE between two unknown wallets was reported. Another data from Santiment shows these whales have been on a selling spree since the first week of April. Despite the growing selling pressure over the token, the trade setup suggests the Dogecoin (DOGE) price is due for a major breakout, which may clear the path towards $0.2.

The short-term price action of Dogecoin suggests the token is stuck within a decisive symmetrical triangle and is ranging along the support to reach the edge of the consolidation. The Stochastic RSI has reached the upper threshold, while the bears are trying to trigger a bearish crossover. The historical pattern suggests that the RSI could remain around the upper threshold for a while, which may help the price to keep up the bullish momentum.

On the other hand, MACD has turned bullish after the selling pressure was outpowered by a notable increase in the buying pressure. With this, the Dogecoin (DOGE) price is expected to rise and test the resistance of the triangle. Meanwhile, the supporting volume has not yet registered, which may reduce the pace of the rally. However, a rise above $0.17 may validate a rise above bearish influence, and until then, the price is expected to remain consolidated within a narrow range.

The post Dogecoin Squeezing Within a Decisive Phase-Here’s the DOGE Price Prediction for the Upcoming Week appeared first on Coinpedia Fintech News

Dogecoin has been among the top-traded tokens, which has been attracting enough liquidity, which has maintained the volatility. Meanwhile, the latest price action has remained stuck within a narrow range, hinting towards a drop in the bullish and bearish pressures. While the spot market remains uncertain, the whales seem to be confident of the upcoming …

BloFin strengthens its position as a global leader in futures trading liquidity and slippage control, outperforming mid-tier competitors and matching the performance of top-tier exchanges.

BloFin Exchange has achieved a significant milestone in future market performance, establishing itself as a top-tier competitor in both liquidity and trade execution quality.

According to the latest official data collected via API monitoring from June 16 to June 19, 2025, BloFin’s futures market depth and slippage performance position the exchange alongside long-established industry leaders such as Binance, OKX, and Bybit, further solidifying its reputation among global futures market participants.

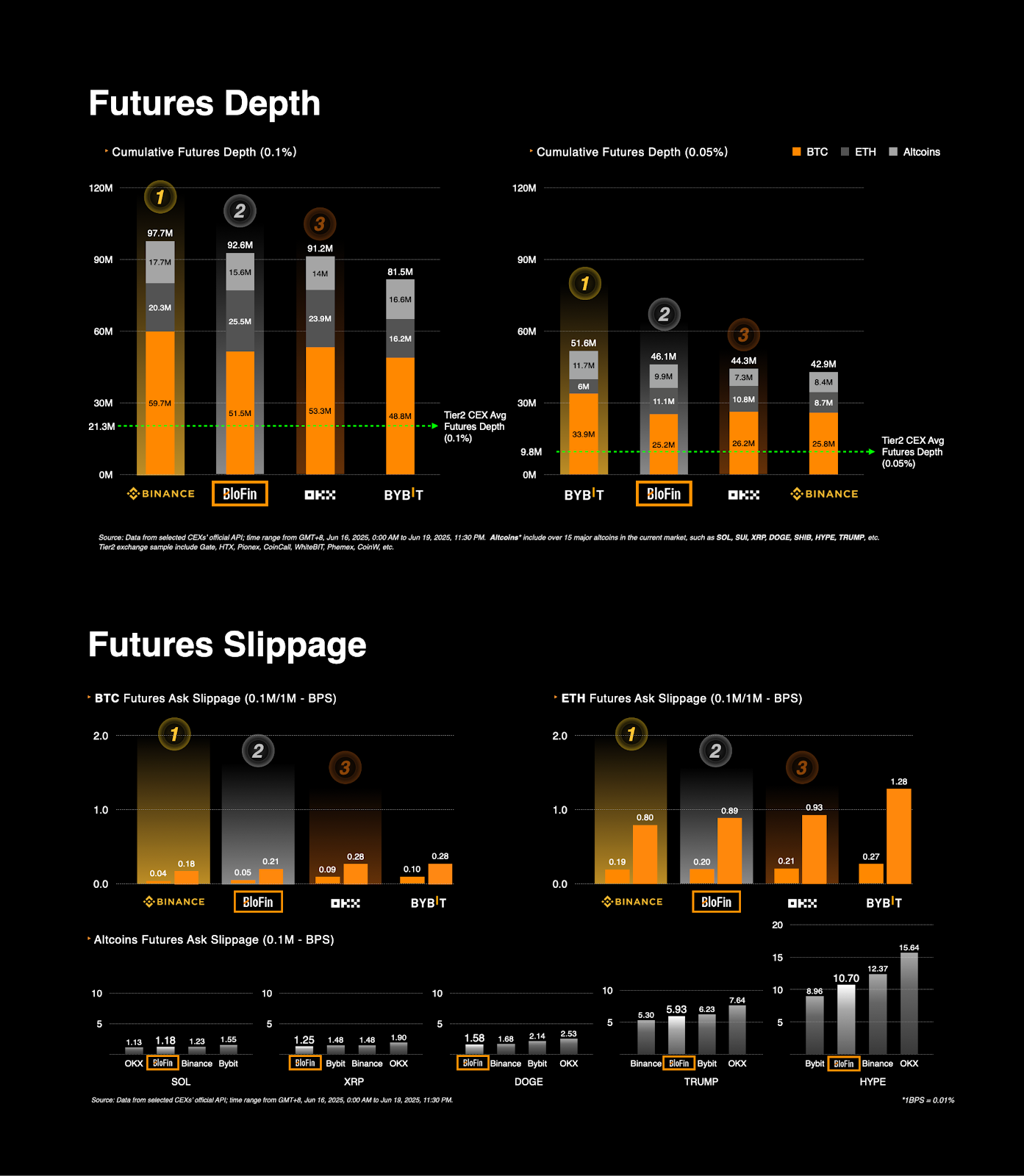

Tier-1 Futures Liquidity Achieved, with a Top-Two Global Ranking Across Depth Metrics

In cumulative futures depth at both the 0.1% and 0.05% price deviation levels, BloFin ranked firmly among the top three global exchanges. Its liquidity performance not only outpaced all mid-tier platforms but also closely matched or exceeded several tier-1 competitors.

At the 0.1% depth level, BloFin secured the second position in overall futures liquidity with a total cumulative depth of 92.6 million, surpassing OKX and coming in just behind Binance.

At the 0.05% depth level, BloFin maintained a strong second-place ranking with a cumulative depth of 46.1 million, outperforming both OKX and Binance under tighter market conditions.

These results demonstrate BloFin’s consistent capacity to support high-volume, low-slippage trading activity for institutional participants and large-volume retail users.

Whale-Grade Slippage Control Delivers Execution Quality on Par with Leading Exchanges

In addition to liquidity depth, BloFin exhibited robust trade execution metrics under stress-tested conditions. The exchange delivered highly competitive slippage rates for both BTC and ETH futures, alongside a wide range of over 15 actively traded altcoins, including SOL, XRP, DOGE, PEPE, ADA, and TRUMP.

BloFin’s slippage performance for major assets under two levels of simulated stress remained in line with top-tier platforms, confirming the exchange’s ability to maintain price stability and execution efficiency in volatile or high-demand trading environments. Notably, BloFin also offered lower slippages for trending, volatile altcoins — an area where many mid-tier competitors face significant execution gaps.

A New Global Contender Reshaping the Futures Trading Landscape

BloFin’s performance in this report affirms its standing as a rising leader in the global futures market. By delivering futures market depth and slippage control on par with tier-1 exchanges, BloFin strengthens its appeal to whales, institutional traders, and high-frequency participants seeking deep liquidity and reliable trade execution across both dominant and emerging digital assets.

As the exchange continues its expansion into key global markets and strategic event sponsorships, this achievement further enhances BloFin’s credibility as a serious futures market contender.

About BloFin

BloFin is a top-tier cryptocurrency exchange that specializes in futures trading. The platform offers 480+ USDT-M perpetual pairs, Coin-Margined Perpetual Contracts, spot trading, copy trading, API access, unified account management, and advanced sub-account solutions. Committed to security and compliance, BloFin integrates Fireblocks and Chainalysis to ensure robust asset protection. By partnering with top affiliates, BloFin delivers scalable trading solutions, efficient fund management, and enhanced flexibility for professional traders. As the constant sponsor of TOKEN2049, BloFin continues to expand its global presence, reinforcing its position as the place “WHERE WHALES ARE MAD