Mantra (OM) is up more than 10% in the past seven days, taking place as the second-largest Real World Asset (RWA) token by market cap. With a market cap of around $6.8 billion, OM is gaining momentum and attracting attention in the RWA space.

Technical indicators are flashing mixed signals, with OM’s RSI cooling off from overbought levels and Ichimoku Cloud structures remaining bullish. As OM trades near key resistance and support zones, traders are watching closely to see if it can extend its rally and set new all-time highs.

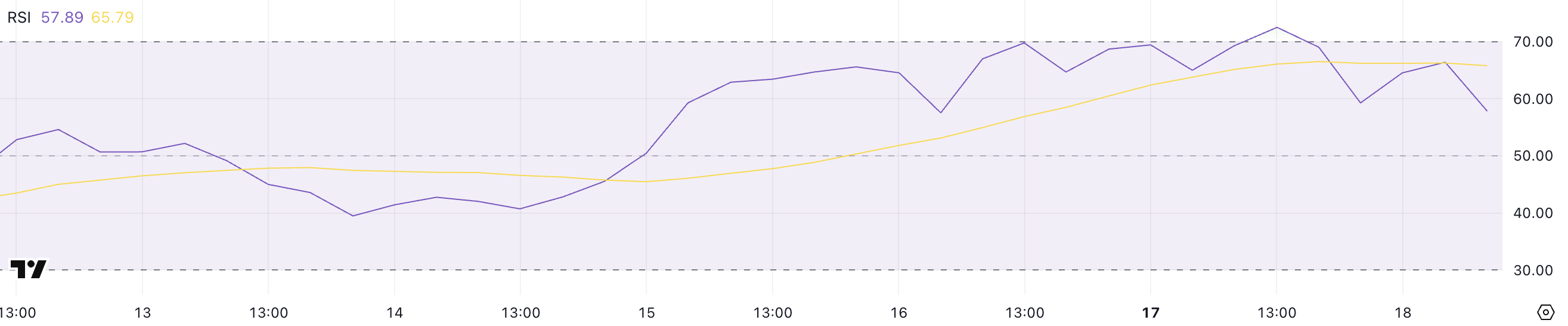

Mantra RSI Is Back To Neutral After Reaching Overbought Levels

Mantra’s Relative Strength Index (RSI) reading is 57.89, maintaining levels above the 50 threshold since March 15.

The RSI briefly reached 72.51 yesterday, signaling that OM approached overbought territory before pulling back slightly.

This sustained move above 50 suggests that OM has been in a bullish phase, with momentum favoring buyers over the past several days.

The RSI is a momentum oscillator that measures the speed and magnitude of recent price movements to evaluate whether an asset is overbought or oversold.

Readings above 70 generally indicate overbought conditions, signaling that an asset could be due for a pullback, while readings below 30 suggest oversold conditions, potentially signaling a buying opportunity.

OM’s RSI at 57.89 suggests that while bullish momentum is still present, it is currently at moderate levels.

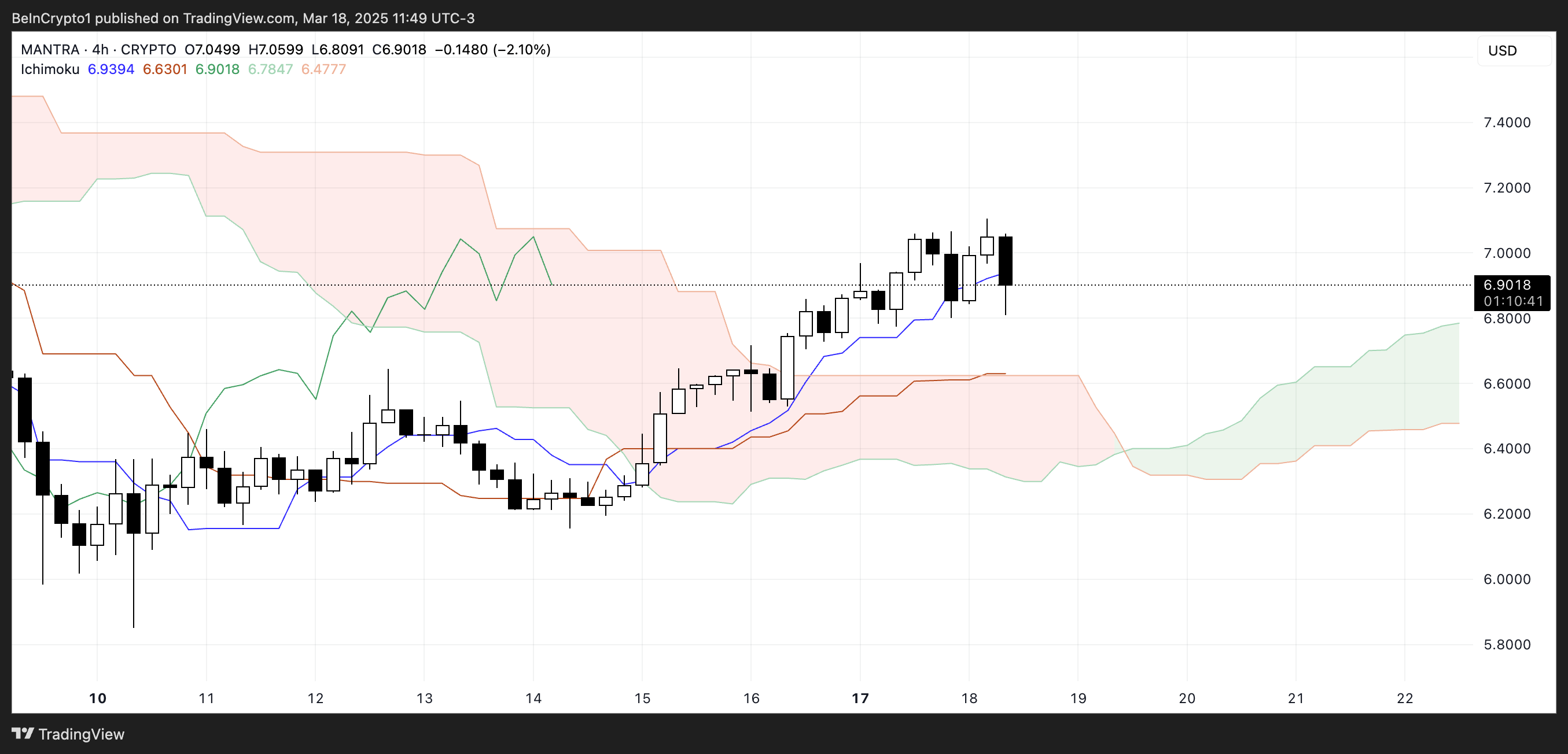

OM Ichimoku Cloud Shows a Bullish Setup

Mantra is currently showing a bullish structure on the Ichimoku Cloud chart.

The price is trading above the cloud, which indicates that the overall trend is still bullish. This solidifies Mantra as one of the biggest RWA coins in the market.

Additionally, the cloud ahead has flipped green, suggesting that if the structure holds, future momentum could continue to favor buyers.

The Tenkan-sen is positioned above the Kijun-sen, reinforcing short-term bullish momentum, although the price recently pulled back after some upward movement.

The Chikou Span is also above the price action and the cloud, supporting the bullish outlook.

However, if the price starts to consolidate or dip toward the Tenkan-sen and Kijun-sen, it could signal a potential pause in momentum or a shift toward a more neutral trend if those levels fail to provide support.

Will Mantra Make New All-Time Highs In March?

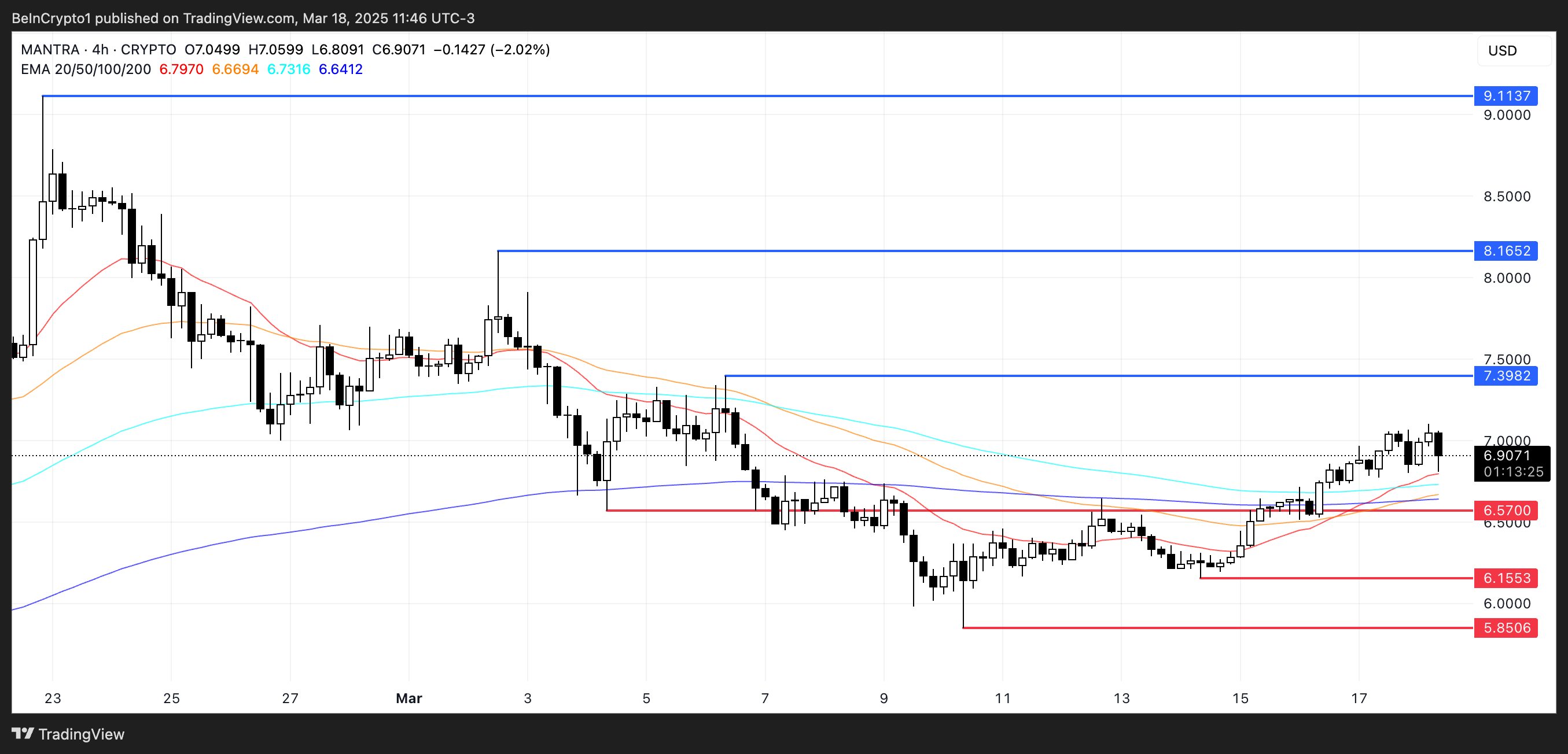

OM’s EMA lines are signaling that a golden cross could soon form, which would strengthen the bullish outlook.

If this pattern is confirmed and Mantra can regain the strong uptrend seen in past months, it could break through the resistance levels at $7.39 and $8.16.

A breakout above these areas could allow OM to test price levels above $9 for the first time ever, potentially setting new all-time highs and possibly making OM surpass Chainlink as the biggest RWA coin in market cap.

On the other hand, if the current bullish momentum fades, OM could decline toward support at $6.57.

A loss of this level could trigger further downside toward $6.15, and if bearish pressure persists, the price could fall as low as $5.85.

The post Mantra (OM) Surges 10% In a Week To Become The Second Biggest RWA Coin appeared first on BeInCrypto.