HOT price may reach a potential peak of about $0.0707 in 2025, based on Coinpedia’s formulated forecast.

The rising adoption and use case expansion of the Holochain will play a crucial role in HOT price action over the next five years.

The future growth prospects of Holo (HOT) coin are heavily dependent on the success of the Holochain’s peer-to-peer, energy efficient platform for decentralized applications. Having existed for more than five years, HOT coin has gained significant traction but the team has to deliver a sustainable and scalable platform to capture a wider share of global DeFi space.

Most importantly, HOT price action in the next five years will heavily depend on the global regulatory environment, led by the United States, Europe, and other major economies.

Holo price may reach a potential peak of about 10 cents in 2026 and a possible low of around $0.001148.

Price Prediction for 2027

Considering the established four-year crypto cycle, diminishing returns, and regulatory outlook, HOT price may reach a potential low of about $0.001630 in 2027 and a possible peak of around 14 cents.

Price Prediction for 2028

As the next Bitcoin-halving year, which also coincides with the next U.S. Presidential election, HOT price may reach a potential peak of about 19 cents and a possible low about $0.002216.

Price Prediction for 2029

If Holo price will have established a rising trend in the prior years, HOT price may reach a peak of about 25 cents in 2029 and a possible low of around $0.002925.

Price Prediction for 2030

By the end of this decade, HOT price may reach a potential peak of about $0.3223 and a possible low of around $0.003685.

Market Analysis

*Predictions below represent respective end of year peaks by the different companies.

2025

2026

2030

Coincodex

$0.000798

$0.000657

$0.00006550

Tradersunion

$0.00101

$0.001179

$0.001877

Pricepredictions

$0.001729

$0.00269

$0.006533

CoinPedia’s Price Prediction

According to Coinpedia’s formulated Holo price forecast for 2025, if the crypto market regains bullish sentiment in the next three quarters, $HOT price will likely end the year at a potential low of about $0.000792, and a possible peak of around $0.0707.

Potential Low

Average Price

Potential High

2025

$0.000792

$0.00386

$0.0707

FAQs

Is HOT a great investment for the next five years?

Yes, it is a potentially profitable investment bolstered by the mainstream adoption of DeFi technology and digital assets.

Top factors that will influence HOT price action by 2030.

The adoption and use case expansion of the Holochain will play a crucial role in HOT price action in the next five years.

Where can you buy HOT tokens?

The HOT coin is listed for trading by Binance, Bybit, Bitget, MEXC, Gate.io, and Crypto.com, among many others.

Will the HOT coin reach $1 by 2030?

With the dubious crypto speculation amid the improving crypto regulatory outlook in major jurisdictions, HOT price could rise to $1 by 2030. However, considering diminishing returns, HOT price may not reach $1 in the next five years.

Regulatory sandboxes have emerged as a concept to drive innovation in a controlled setting. They allow companies to test new crypto products and services while regulators observe and adapt regulations. While jurisdictions like the UK, the UAE, and Singapore have already created sandboxes, the US has yet to create one at the federal level.

BeInCrypto spoke with representatives of OilXCoin and Asset Token Ventures LLC to understand what the US needs to build a federal regulatory sandbox and how it can unify a fragmented testing environment for innovators.

A Patchwork Approach

As the name suggests, regulatory sandboxes have emerged as a tool for providing a controlled testing ground. This environment allows entrepreneurs, businesses, industry leaders, and lawmakers to interact with new and innovative products.

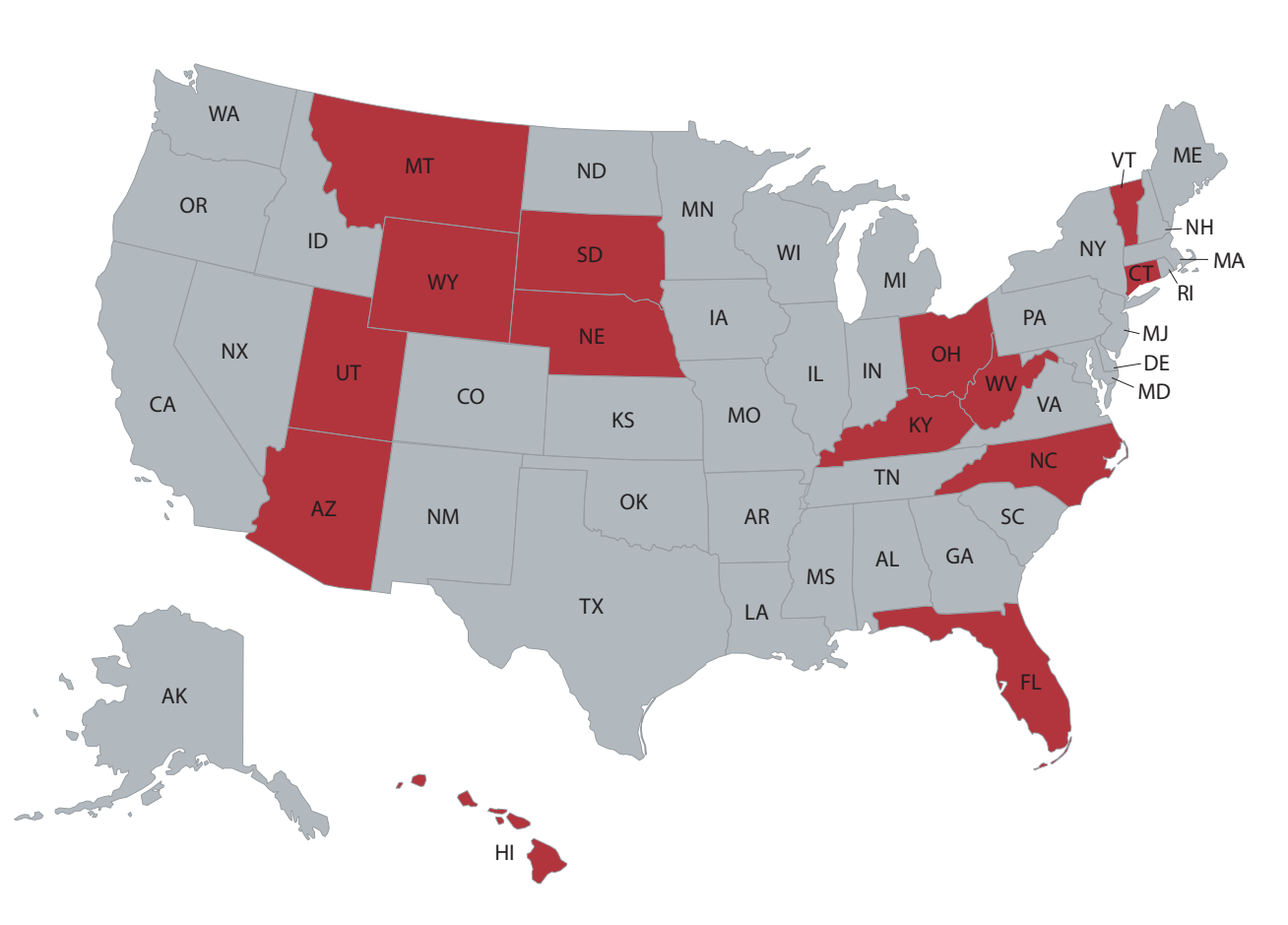

According to the Institute for Reforming Government, 14 states in the United States currently have regulatory sandboxes for fintech innovation.

Of those, 11 are industry-specific and cover other sectors like artificial intelligence, real estate, insurance, child care, healthcare, and education.

Utah, Arizona, and Kentucky are the only jurisdictions among these states with an all-inclusive sandbox. Meanwhile, all but 12 states are currently considering legislation to create some regulatory sandbox for innovation.

Due to its relatively short existence, the crypto market has underdeveloped legislation. While state-level sandboxes enable innovators to demonstrate their products’ capabilities to the public, they are significantly constrained by the lack of federal regulatory sandboxes.

The Need for Federal Oversight

Though statewide efforts to create regulatory sandboxes are vital for innovation, entrepreneurs and businesses still face constraints in developing across borders or reaching an audience at a national level.

Rapid advancements in fields like blockchain and artificial intelligence (AI) add a particular layer of uncertainty, given that existing legal frameworks may not be well-suited to these technologies.

At the same time, regulators may face difficulties in developing appropriate rules for these technologies due to a potential lack of familiarity with these constantly changing industries.

As a result, industry participants are increasingly calling for creating a federal regulatory sandbox. This environment could be a collaborative framework to address the gap, facilitating communication and knowledge sharing between regulators and industry stakeholders.

“The implementation of a federal regulatory sandbox in the United States has the potential to significantly enhance both innovation and regulatory oversight by reducing the uncertainties often associated with navigating the regulatory landscape across state lines. Such an initiative could help establish a coherent framework characterized by uniformity, continuity, and a conducive environment for innovation,” said Paul Talbert, Managing Director of ATV Fund.

According to Rademacher and Talbert, this proposal would meet the needs of all players involved.

Benefits of a Federal Regulatory Sandbox

A sandbox provides innovators with a controlled environment to test products under regulatory oversight without the immediate burden of full compliance with rules that may not yet fit their technology.

It also allows regulators to acquire firsthand insights into blockchain applications, facilitating the creation of more knowledgeable and flexible regulatory policies.

“Startups should have clear eligibility criteria to determine their qualification for participation, while regulators must outline specific objectives—whether focused on refining token classification frameworks, testing DeFi applications, or improving compliance processes,” Rademacher said.

It could also help the United States reinforce its position as a leader in technological innovation.

“By fostering innovation through simplicity, regulatory certainty, and conducive environments, the United States can significantly strengthen its competitive position in the global fintech landscape,” Talbert added.

While the United States has stalled in creating a federal framework for fintech innovation, other jurisdictions around the world have already gained significant ground in this regard.

Global Precedents

The Financial Conduct Authority (FCA), which regulates the United Kingdom’s financial services, launched the first regulatory sandbox in 2014 as part of Project Innovate. This initiative aimed to provide a controlled environment for testing innovative products.

The government asked the FCA to establish a regulatory process to promote new technology-based financial services and fintech and ensure consumer protection.

The United Arab Emirates (UAE) and Singapore, in particular, have made progressive strides in creating federal regulatory sandboxes.

The UAE, for example, currently has four different sandboxes: the Abu Dhabi Global Market (ADGM) Regulation Lab, the DSFA Sandbox, the CBUAE FinTech Sandbox, and the DFF Regulation Lab.

Their focus areas include digital banking, blockchain, payment systems, AI, and autonomous transport.

Meanwhile, the Monetary Authority of Singapore (MAS) launched its Fintech Regulatory Sandbox in 2016. Three years later, MAS also launched the Sandbox Express, providing firms with a faster option for market testing certain low-risk activities in pre-defined environments.

“The success of regulatory sandboxes in jurisdictions such as the United Kingdom, Singapore, and the United Arab Emirates has highlighted the importance of key attributes: regulatory collaboration, transparent processes, continuous monitoring, and the allocation of dedicated resources. As a result, a growing number of jurisdictions worldwide are looking to replicate the frameworks established by these pioneering countries to strengthen their competitive position in the global fintech landscape,” Talbert said.

Rademacher believes these jurisdictions’ innovations should prompt the United States to accelerate its progress.

For that to happen, the United States must overcome certain hurdles.

Challenges of a Fragmented US Regulatory Landscape

A fragmented network of federal and state agencies overseeing financial services presents a key challenge to establishing a US federal regulatory sandbox.

“Unlike other countries with a single financial authority overseeing the market, the U.S. has multiple agencies—including the SEC, CFTC, and banking regulators—each with different perspectives on how digital assets should be classified and regulated. The lack of inter-agency coordination makes implementing a unified sandbox more complex than in jurisdictions with a single regulatory body,” Rademacher told BeInCrypto.

Yet, in recent years, important SEC and CFTC actors have expressed interest in adopting a more favorable regulatory approach to innovation.

“Even though I tend to be more of a beach than a sandbox type of regulator, sandboxes have proven effective in facilitating innovation in highly regulated sectors. Experience in the UK and elsewhere has shown that sandboxes can help innovators try out their innovations under real-world conditions. A sandbox can provide a viable path for smaller, disruptive firms to enter highly regulated markets to compete with larger incumbent firms,” Peirce said in a statement last May.

However, the full scope of national regulations far exceeds the authority of these two entities.

Congressional and Constitutional Hurdles

Any legislative measure to develop a federal regulatory framework for sandboxes in the United States would have to undergo Congressional approval. Talbert highlighted several potential constitutional dilemmas the promotion of an initiative of this nature may face.

“These dilemmas include issues related to the non-delegation doctrine, which raises concerns about the constitutionality of delegating legislative power; equal protection considerations under the Fifth Amendment’s Due Process Clause; challenges arising from the Supremacy Clause; and implications under the Administrative Procedure Act (APA) and principles of judicial review,” he said.

To address these complexities, Congress must enact clear legal boundaries that ensure a regulatory framework is both predictable and open. Given the current administration’s emphasis on technological innovation, the prospects for creating a sandbox appear positive.

“Given the current composition of Congress, which aligns with the political orientation of the new executive branch, there may be a timely opportunity for regulatory reform. Such reform could facilitate the creation of a cohesive federal regulatory framework and enhance collaboration among federal agencies,” Talbert told BeInCrypto.

However, creating a federal regulatory sandbox is not a one-size-fits-all solution.

Balancing State Autonomy and Federal Regulations

State autonomy is enshrined in the US Constitution. This protection means that, even though a regulatory sandbox may exist at the national level, individual states still have the authority to restrict or prohibit sandboxes within their jurisdictions.

Encouragingly, most US states are already exploring regulatory sandboxes, and the states that have already implemented them represent diverse political viewpoints.

However, other considerations beyond political resistance must also be addressed.

“A federal regulatory sandbox might also face opposition from established financial institutions, including banks, which may perceive potential threats to their existing business models. Furthermore, federal budgetary constraints could impede the government’s capacity to support the development and maintenance of a federal regulatory framework,” Talbert added.

Effective federal regulations will also require a balance between businesses’ concerns and regulators’ responsibilities.

“The two biggest risks are overregulation—imposing excessive restrictions that undermine the sandbox’s purpose—or underregulation, failing to provide meaningful clarity. If the rules are too restrictive, businesses may avoid participation, limiting the sandbox’s effectiveness. If they are too lax, there is a risk of abuse or regulatory arbitrage. A well-executed federal regulatory sandbox should not become a bureaucratic burden but rather a dynamic framework that fosters responsible growth in the digital asset space,” Rademacher told BeInCrypto.

Ultimately, the best approach will require coordination from different governing bodies, industry stakeholders, and bipartisan collaboration.

Fostering Collaboration for a Successful Sandbox

Due to recent strained communication between tech and federal agencies, Rademacher believes fostering a cooperative atmosphere is essential for creating a functional federal sandbox.

“The approach must be collaborative rather than adversarial. Agencies should view the sandbox as an opportunity to refine regulations in real time, working alongside industry participants to develop policies that foster responsible innovation. Involvement from banking regulators and the Treasury Department could also be valuable in ensuring that digital assets are integrated into the broader financial system in a responsible manner,” he said.

Achieving this requires a bipartisan approach to harmonizing regulatory goals and setting clear boundaries. Industry collaboration with lawmakers and regulators is vital to showing how a sandbox can promote responsible innovation while safeguarding consumers.

“Its success will ultimately depend on whether it serves as a bridge between innovation and regulation, rather than an additional layer of complexity,” Rademacher concluded.

In a significant development, the Bank of Korea has unveiled its central bank digital currency (CBDC) pilot program, dubbed “Digital Test Project Hangang.” The Bank of Korea, in partnership with seven major banks, is set to launch the pilot program next month, with a planned duration of about three months.

Notably, the Bank of Korea intends to test the efficiency and feasibility of a CBDC-based payment system via the Hangang program. The partnering banks will issue deposit tokens for use at various retail outlets, including local supermarkets, online shopping platforms, and convenience stores.

Bank of Korea Launches CBDC Program: What To Know

According to local reports, the Bank of Korea will debut a real-world CBDC pilot program in April, possibly involving 100,000 local citizens. This trial will enable participants to exchange bank deposits for “deposit tokens” and make payments at partner merchants.

Significantly, Hangang, expected to begin in April, will possibly last for about three months. In collaboration with seven major banks, including KB Kookmin, Shinhan, Hana, Woori, NH Nonghyup, IBK Industrial Bank of Korea, and BNK Busan, the BoK will examine the potential of its CBDC for real-world transactions. Commenting on the development, a BoK official stated,

Through deposit token payments, merchants can receive settlement funds in real time. Additionally, related transaction fees are expected to be reduced by minimizing intermediary institutions in the payment process.

Beyond Traditional Finance: Unveiling the Potential of CBDCs

Through the Hangang CBDC program, the Bank of Korea intends to test the feasibility of CBDCs for real-world transactions. The BoK intends to replace the traditional payment methods with digital currencies, specifically CBDCs. Thus, the Hangang pilot program will serve as a trial.

If the Bank of Korea introduces an “institutional digital currency,” the other banks involved in the program will issue linked tokens. This process will enable consumers to use these tokens for payments. Participants in the pilot program can convert their bank deposits into deposit tokens and vice versa, allowing for seamless transactions. The central bank is expected to release a public announcement by the end of this month to recruit eligible participants.

Meanwhile, South Korea has strengthened its anti-money laundering regulations to tackle the growing crypto threats.

Will South Korea Establish a Strategic Bitcoin Reserve?

Recently, the Bank of Korea dismissed the possibility of adopting a strategic Bitcoin reserve. The bank cited price volatility and inherent risks of cryptocurrencies as a major reason. The BoK stated, “In the case of cryptocurrency market instability, transaction costs to cash out Bitcoins could rise drastically.”

This comes amid speculations of North Korea’s potential Bitcoin reserve plans as the country’s notorious Lazarus Group accumulates Bitcoin. Reportedly, North Korea flipped Bhutan and El Salvador in BTC holdings, becoming the fourth largest holder of Bitcoin.

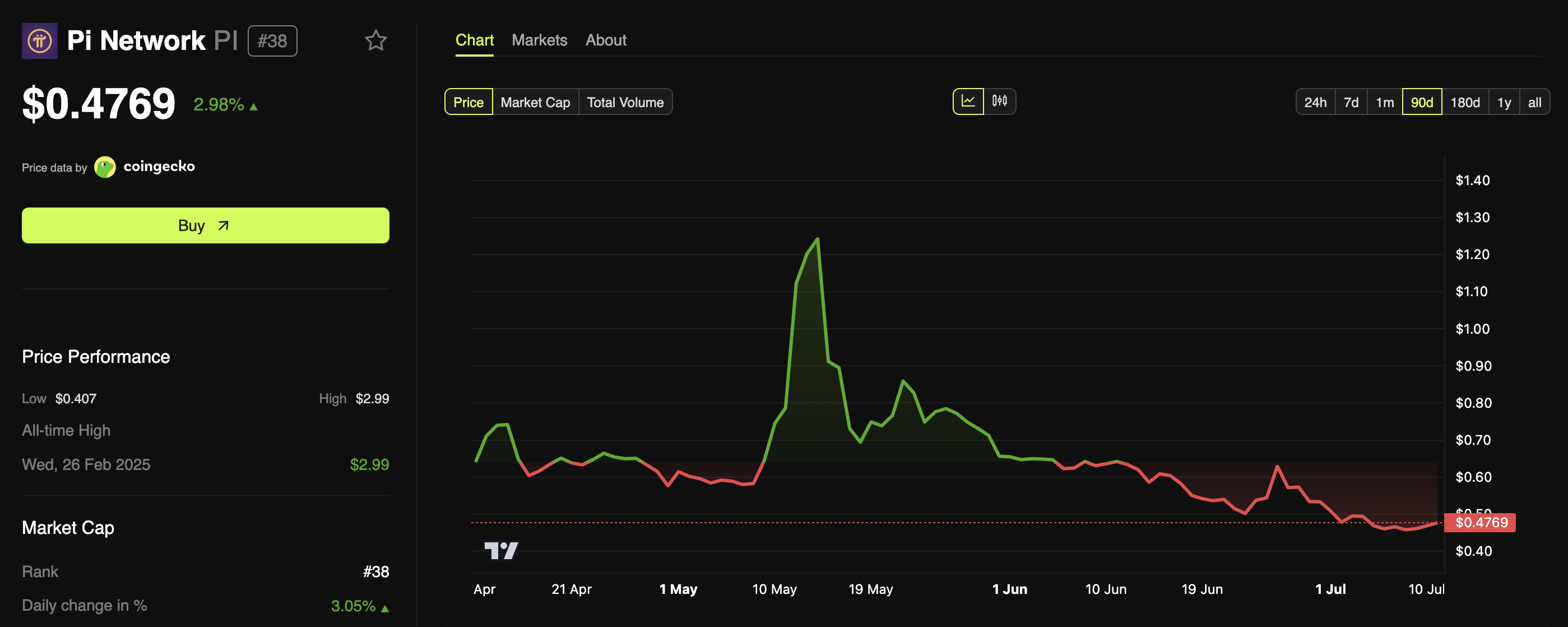

The Pi Network has achieved a significant milestone, with over 12,000 applications created on its newly launched Pi App Studio platform in less than two weeks.

This achievement coincides with a roughly 3% increase in the price of Pi Coin (PI) over the past day. However, an expert warns that the PI may face challenges ahead unless the team implements some major changes.

This ease of use has made it popular among users, as a prominent Pioneer, Dr Altcoin, highlighted recently.

“The new Pi App submissions for the AI App Studio have surpassed 12,000!” the user posted.

Dr. Altcoin suggested that Pi Network has the potential to become the largest crypto project in history, even if only half of the submitted dApps are fully functional and approved. He pointed to several factors driving this potential.

These include Pi Network’s large KYC-verified user base, broad global reach in over 200 countries and regions, and distinctive requirement for KYB approval from centralized exchanges and businesses using Pi. Additionally, Pi Network leads the industry with the highest number of community-developed dApps.

“All of this will organically and significantly boost the price of Pi in the years ahead,” the Pioneer noted.

What Does Pi Coin Price Need to Recover?

Meanwhile, PI has shown signs of recovery. BeInCrypto data showed that the price rose 2.98% over the past day. At press time, Pi Coin’s trading price was $0.47.

However, the uptick is not due to Pi App Studio’s popularity but rather a market-wide rally driven by Bitcoin’s new record high. Furthermore, the small gains seem hardly enough to bring PI out of its nearly two-month-long slump.

Pi Coin’s price is just 16% away from its all-time low, and an expert claimed that it is ‘doomed to collapse below $0.40.’ Nevertheless, the Pioneer outlined several actions the team can take to save this sinking ship.

“If PCT (Pi Core Team) implements just 2 of the following 11 actions, the community can regain confidence, and the price can steadily rise again,” Pi Barter Mall stated.

Some of the strategies outlined include releasing a clear mainnet launch timeline, introducing DAO governance, and implementing token burn and buy-back programs. The user also proposes restarting mining rewards, providing incentives, launching liquidity pools, lending, staking, and cross-chain compatibility.

Furthermore, Pi Barter Mall stressed the importance of restoring user trust by sharing team holdings and addressing previous KYC restrictions.

“Without real action, Pi will lose the final layer of trust. But if PCT chooses the right path, we could witness a historic reversal,” the user concluded.

Previously, Ray Youssef, CEO of NoOnes, shared a similar perspective on Pi Network’s future. He emphasized that its success hinges on the team’s ability to move beyond the hype and focus on execution. The executive highlighted the importance of transitioning to an open mainnet, allowing free trading on public blockchains.

Youssef noted that this shift would enable price discovery and greater participation, key elements for the network’s long-term growth and sustainability.

“For Pi to sustainably reach or exceed $10 in a real market, it will need to have a full mainnet launch with open transfers, listings on high liquidity exchanges, a real economic layer, where people use Pi to buy, sell, or pay for services, and controlled inflation to ensure newly unlocked tokens don’t flood the market,” Youssef told BeInCrypto.

Thus, while the team continues to roll out new apps and updates, it still needs to go beyond these surface-level improvements and focus on the fundamentals to drive real price rally and sustainable growth for the network.