Binance will temporarily suspend ETH and related Layer 2 token transfers on May 7 to support Ethereum’s upcoming Pectra Upgrade. This pause is scheduled to maintain smooth operations while technical adjustments are made to the Ethereum network.

The suspension will begin at 09:45 UTC, which is about 20 minutes before the upgrade time of 10:05 UTC. Binance stated that the trading of all unaffected tokens will continue as usual during this window, and no user action is required.

ETH and L2 Token Transfers Temporarily Suspended

The pause will affect deposits and withdrawals of tokens on Ethereum and popular Layer 2 networks. These tokens include Arbitrum, Optimism, zkSync Era, Base, Manta, Starknet, Polygon, Metis, Scroll, and Celo, among others. This is a routine safety measure to make sure that users’ funds are not at risk during changes to the network infrastructure.

The exchange has mentioned that it will handle all technical requirements associated with the upgrade and will reopen withdrawals and deposits once the networks are stable. No additional announcement will be made as and when the services resume.

What the Ethereum Pectra Upgrade Brings

The Pectra Upgrade is one of Ethereum’s most anticipated updates since the Merge. It merges changes from both the Prague and Electra development tracks to improve usability, scalability, and Layer 2 efficiency. Among the major changes are cheaper Layer 2 transactions, increased validator caps, smarter wallet interactions, and improvements to developer tooling.

The Ethereum Pectra Upgrade brings lower L2 fees, smart wallets, and a lot to the network. Ahead of the update, Ethereum’s price resilience is near $1,800 and has created speculation about a bullish breakout following the upgrade. Analysts suggest that if the Pectra hype delivers, ETH could retest $2,000 levels.

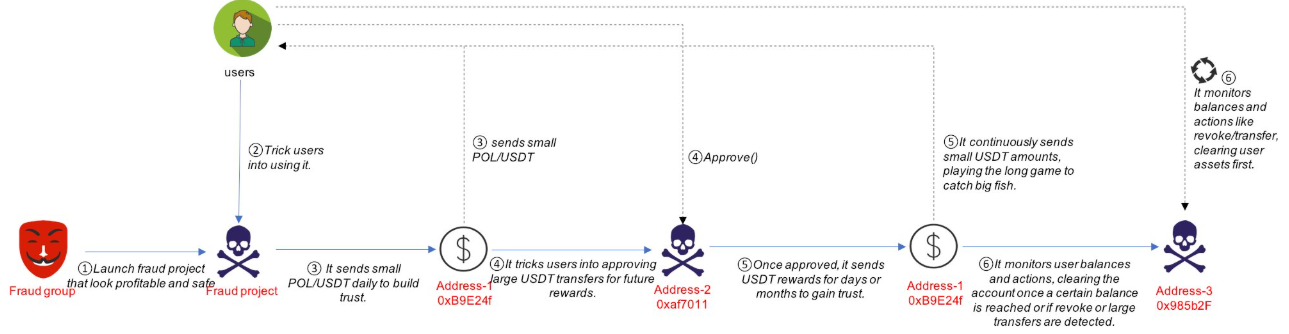

GoPlus Security unveiled the latest playbook employed by a well-coordinated scam network targeting unsuspecting crypto users with promises of effortless USDT earnings.

Meanwhile, deepfake AI is progressively becoming a concern. Bad actors leverage authoritative voices in the industry to target unsuspecting victims. These mark an alarming disclosure that mirrors the growing sophistication of crypto fraud.

These projects entice users with the promise of “zero-cost, stable USDT rewards” in exchange for completing simple, low-effort tasks. Once initial contact is established, scammers send small tokens and minimal USDT over several days to establish legitimacy. But it’s all a calculated ruse.

The ultimate goal is to convince users to grant token approval permissions, often to externally owned accounts (EOAs). Once approvals are in place, the scammers continue sending rewards for days or weeks while monitoring wallets.

When a user’s balance crosses a threshold or revocation activity is detected, high-speed front-running bots swoop in and drain funds in seconds. These trading bots are willing to burn gas at any cost.

“This is a long game to catch big fish,” GoPlus warned in its statement.

Against this backdrop, GoPlus Security cautions against granting unlimited token approvals, especially to EOAs. The firm also urges users to adopt proactive on-chain security tools.

“There’s no such thing as free money — don’t trust projects that claim you can easily earn just by participating,” it added.

As BeInCrypto reported, these range from verifying token contracts and approval histories to using tools that limit permissions or automatically revoke dormant approvals.

Deepfake Deception: The Next Frontier of Crypto Fraud

Beyond blockchain, crypto scams are exploiting artificial intelligence at a dangerous scale. Bad actors also weaponize deepfake technology, which creates convincingly fake videos of public figures, to defraud investors.

In a warning earlier this year, Binance co-founder Changpeng Zhao (CZ) revealed AI-generated clips promoting fake investment platforms falsely endorsed by major crypto personalities.

“There are deepfake videos of me on other social media platforms. Please beware,” CZ stated.

A disturbing example recently emerged in Ghana. The country’s Ashesi University denounced a deepfake impersonation of its president, Patrick Awuah Jr. Reportedly, scammers used him to promote a scam called “Crypto Klutz.”

They embedded the video in a fake news article mimicking Graphic Online. The scammers circulated it alongside doctored X screenshots to manufacture credibility.

“…Neither Patrick Awuah nor Ashesi University is associated with this or any similar platform. Please help protect our community by reporting it as fraudulent when encountered and encourage others who see it to do the same,” the university articulated.

It cited too-good-to-be-true promises, fake celebrity endorsements, and non-existent exchanges or wallets. Other red flags include urgency tactics to rush decisions, and demands for private keys or upfront payments.

A Variety report confirmed that deepfake-assisted fraud surpassed $200 million in losses in Q1 2025 alone. This figure highlights how fast scammers scale operations through generative AI and synthetic media.

As on-chain scams become more patient and AI deepfakes more persuasive, the crypto community faces a dual-threat environment unlike anything seen before.

“AI-powered scams are changing the crypto game. With deepfakes, voice cloning, and AI-generated phishing, scammers are raking in millions,” trader Crypto Frontline remarked.

US President Donald Trump has continued to pressure Fed Chair Jerome Powell and the committee to lower rates from the benchmark 4.25% to 4.5%. This time around, the president has gone as far as sending a handwritten note to Powell, which contained a breakdown of how other countries have lower rates, in a bid to

IRS demands Coinbase data to combat crypto tax evasion; user claims Fourth Amendment violation.

Supreme Court decision could reshape privacy rights for millions of crypto users nationwide.

The U.S. government is urging the Supreme Court to dismiss a legal challenge from James Harper, a Coinbase user who claims the IRS violated his constitutional rights by accessing his crypto transaction data. The case touches on a broader debate: do Americans have a right to privacy when it comes to their crypto activity?

Background: IRS Targets Crypto Tax Evasion

This dispute traces back to a 2016 investigation, where the IRS suspected widespread underreporting of crypto-related income. As part of its probe, the agency issued a court-approved summons to Coinbase, requesting information on high-volume users—including Harper.

The IRS has since argued that such records are crucial in enforcing tax compliance and identifying unreported gains in the fast-evolving crypto space.

Harper’s Argument: A Constitutional Overreach?

Harper contends that the IRS violated his Fourth Amendment rights, which protect U.S. citizens from unreasonable searches and seizures. His legal team argues that obtaining detailed financial data without individual suspicion constitutes government overreach into personal digital finance.

Legal analysts note that this case could become a landmark in defining digital financial privacy. “The Fourth Amendment was written before the internet, but its spirit is very much alive in cases like this,” one privacy attorney told [news source].

U.S. Government’s Response: No Privacy Over Third-Party Records

In a recent filing, Solicitor General D. John Sauer responded that Harper voluntarily provided his data to Coinbase, and therefore waived any reasonable expectation of privacy.

The government pointed to legal precedents like U.S. v. Miller, which held that financial data held by third parties—such as banks—do not receive the same constitutional protections. Coinbase’s user agreement, the filing argues, also clearly states that the company may cooperate with law enforcement when required.

What’s at Stake: Financial Privacy in the Age of Crypto

So far, lower courts have sided with the IRS, viewing Coinbase’s records as business data rather than private papers. If the Supreme Court agrees, it could effectively give the green light for broader government access to user data stored on crypto platforms.

Legal takeaway: A ruling in favor of the IRS could set a precedent that weakens digital privacy protections for millions of crypto users in the U.S., not just those suspected of wrongdoing.

Final Thought

While this case may seem narrow, its implications could be broad and long-lasting. At its heart is a fundamental question: does the U.S. Constitution protect crypto financial records the same way it does your personal files and papers?

With the Supreme Court yet to weigh in, the future of digital privacy in crypto hangs in the balance.

Never Miss a Beat in the Crypto World!

Stay ahead with breaking news, expert analysis, and real-time updates on the latest trends in Bitcoin, altcoins, DeFi, NFTs, and more.

The post IRS vs. Coinbase: Supreme Court Asked to Reject Crypto Privacy Challenge appeared first on Coinpedia Fintech News

Story Highlights IRS demands Coinbase data to combat crypto tax evasion; user claims Fourth Amendment violation. Supreme Court decision could reshape privacy rights for millions of crypto users nationwide. The U.S. government is urging the Supreme Court to dismiss a legal challenge from James Harper, a Coinbase user who claims the IRS violated his constitutional …