In a convoluted and dramatic scandal, HyperLiquid was rocked today by a massive JELLY short squeeze. It was forced to assume one trader’s liabilities, leaving it on the hook for $230 million.

As this situation developed, major CEXs like Binance and OKX listed JELLY perpetuals in what looks like a direct attack. HyperLiquid delisted the token, sparking extreme controversy.

Essentially, massive JELLY whales managed to manipulate the meme coin price, causing losses in HyperLiquid’s HLP vault.

“A massive whale with 124.6 million JELLYJELLY ($4.85 million) is manipulating its price to make Hyperliquidity Provider (HLP) face a loss of $12 million. He first dumped the token, crashing the price and leaving HLP with a passive short position of $15.3 million. Then he bought it back, driving the price up—causing HLP to suffer a loss of nearly $12 million,” LookonChain claimed via social media.

So, essentially, JELLY JELLY initially surged nearly 500% today. This dramatic jump was sparked by what’s called a “short squeeze.” It occurs when someone bets heavily that a coin’s price will fall (known as “shorting”), but instead, the price unexpectedly rises.

In this case, a trader borrowed a massive amount of JELLY tokens and sold them immediately. He expected the price to drop, buy the tokens back cheaper, and keep the difference as profit.

Unfortunately for the trader, the price didn’t fall—it skyrocketed, forcing them to buy back the coins at much higher prices, creating massive losses.

This sudden forced buying pushed the price even higher, catching the attention of traders and investors who jumped in to ride the wave. In under an hour, JELLY’s market cap rapidly increased from $10 million to $43 million.

This frenzy also left Hyperliquid, the exchange involved, holding a big loss of $6.5 million from the trader’s failed short position, sparking speculation about potential financial stress on the platform.

Meanwhile, Binance and OKX listed JELLY perpetuals, further driving its price up. So the potential loss became even larger for Hyperliquid. Some users even urged Binance and other competitors to list the token and deal a ‘death blow’ to Hyperliquid.

Binance Users Urging Officials to List JELLY JELLY and Trigger Losses for Hyperliquid. Source: X (formerly Twitter)

Binance is Apparently Trying to Liquidate HyperLiquid

In a very interesting twist, it looks like these competitors are heeding the call. Binance, the world’s largest crypto exchange, was hit with a wave of requests to list JELLY JELLY, thereby causing big losses for HyperLiquid.

Yi He, one of its co-founders, said she would consider a listing, and crypto sleuth ZachXBT claimed that the original whale was funded via Binance.

Shortly after these developments happened, Binance announced that it would begin offering perpetuals contracts for JELLY.

OKX also jumped on the bandwagon with perpetuals trading of its own. After this, HyperLiquid announced that it would delist JELLY JELLY, seemingly erasing its unrealized losses.

“After evidence of suspicious market activity, the validator set convened and voted to delist JELLY perps. All users apart from flagged addresses will be made whole from the Hyper Foundation. This will be done automatically in the coming days based on onchain data. There is no need to open a ticket. Methodology will be shared in detail in a later announcement,” HyperLiquid’s statement claimed.

This radical action immediately caused an explosion on social media. HyperLiquid’s supporters expressed unease over the JELLY JELLY incident, while its detractors accused the firm of criminal activity.

The firm’s validators confirmed that they unanimously took the decision, partially rebutting rumors that its CEO acted alone.

Still, there are no mincing words here. If HyperLiquid can simply declare its JELLY JELLY liabilities null and void, that’s a highly destabilizing act.

The way it handled the $JELLY incident was immature, unethical, and unprofessional, triggering user losses and casting serious doubts over its integrity. Despite presenting itself as an innovative decentralized exchange with a…

In an exclusive interview with BeInCrypto, former US CFTC Commissioner Timothy Massad explains how President Trump’s crypto ventures and political power have significantly overlapped in his first two months at the White House.

Shortly before assuming office for the second time, US President Donald Trump dove head-first into a flurry of crypto experiments. From endorsing World Liberty Financial (WLFI) to launching his meme coin, Trump is raising serious concerns over conflicts of interest. Tim Massad, the 12th CFTC Chairman, who served under Barack Obama, shares his thoughts.

A Historic President For Many Reasons

Before assuming his first term in office in 2016, President Trump broke with modern precedent by departing from established conflict-of-interest norms. A real estate mogul with a trademark for a last name, Trump would be entering the Oval Office as the leader of a multi-billion dollar empire.

While former presidents like Jimmy Carter and George W. Bush took measures to separate themselves from their businesses by placing their assets in a blind trust, the sitting President took a different approach.

Instead, Trump handed day-to-day management decisions over to his sons but did not divest in his ownership stake.

Though he received much backlash during his first term over conflict of interest concerns, Trump refused to relinquish ownership of the Trump Organization before assuming office for the second time.

Given Trump’s favorable stance toward digital asset policy development, players inside and outside the industry have begun to wonder whether his decisions are based on the sector’s best interests or are designed to benefit his own ventures.

How Deep is Trump’s Involvement in World Liberty Financial?

Though Trump does not have a direct role in WLFI, he appears on the whitepaper’s list of supporting teams as “Chief Crypto Advocate.” His three sons, Eric, Donald Jr., and Barron, are also on the list.

Reports further unveiled that the Trump family holds a 75% stake in the platform’s net revenue and a 60% stake in the holding company. At the same time, Trump and his associates own 22.5 billion of the company’s tokens.

For former CFTC Commissioner Tim Massad, despite Trump’s informal role in WLF’s governance, his stake in the platform’s performance raises serious conflicts of interest.

“I think it’s unprecedented and plainly wrong for a President of the United States to engage in commercial ventures or have his family and associates engage in commercial ventures that can be directly influenced by the policies he adopts as President or the statements he makes about those policies,” Massad told BeInCrypto.

Meanwhile, the tokens themselves are non-transferrable, limiting financial flexibility. Though the project aims to provide token holders access to a range of DeFi-related products and services, it has yet to launch them. In the meantime, token holders will have to wait until the time comes to use their tokens.

“I have yet to see any real business case or utility that’s of value to people who invest. So I think it all just has a character of taking advantage of people,” Massad added.

The industry has also grown weary over how WLF and other Trump-endorsed projects could be used to gain the President’s favor.

Industry Leaders Voice Concerns Over World Liberty Financial’s Legitimacy

Shortly before Trump launched World Liberty Financial, many prominent figures in the crypto sector warned that the project could cause Trump further legal troubles. Meanwhile, Alex Miller, CEO of Web3 platform Hiro, described the project as an “obvious pump scheme.”

Meanwhile, Alex Miller, CEO of Web3 platform Hiro, described the project as an “obvious pump scheme.”

Just fucking shoot me

Anyone who thinks this is good for crypto, that it doesn’t make us look like clowns, that it doesn’t set us back YEARS in credibility….

This is such an obvious pump scheme. Maybe he won’t literally rug but he’s just grifting and it’s pathetic pic.twitter.com/8bTGmUfLvG

Other industry leaders, such as Mark Cuban, Max Keiser, and Anthony Scaramucci, also criticized Trump’s decision to proceed with WLF’s token sales. Trump’s involvement in the project heightened fears that crypto’s fragile public image and controversial reputation would be smeared further.

Massad agreed with this last point, adding that crypto policy development is alive and well today more than ever. The ongoing development of stablecoin regulations, open talks of a national crypto strategic reserve, and a Senate-driven digital asset working group are only some of the current institutional initiatives.

“He, the Trump Organization and his family members should not be engaging in commercial ventures that pose such blatant conflicts of interest, given the fact that crypto regulation and things like a potential Bitcoin reserve are important policy issues today. A US president shouldn’t be engaging in these things at all, in my view,” Massad said.

Since the project’s launch six months ago, several examples validating these concerns have emerged. The most notable one has focused on Tron founder Justin Sun.

The move was highly controversial. Despite Trump’s endorsement, WLFI struggled to meet its $30 million fundraising target during its first public sale. The token’s availability was restricted, excluding general trading and limiting purchases to non-US and accredited US investors.

Sun’s investment turned WLFI’s luck around. Soon after that, he also became one of the project’s advisors. Then, on the day of Trump’s inauguration, Sun invested an additional $45 million in the project, bringing the total sum to $75 million.

This investment brought varying degrees of scrutiny. While some questioned his quick transition from investor to advisor, others pointed to Sun’s past as a potential motive for his contributions.

In March 2023, the SEC filed fraud charges and other securities law violations against Sun and his companies. This regulatory baggage has led some industry leaders to question the wisdom of his association with World Liberty Financial.

Meanwhile, Tron’s price soared following Sun’s latest WLF investment. Tron, which had been experiencing lagging prices up until that point, was able to jumpstart its trading activities.

TRON Price Surge Following Sun’s $45 Million Investment in World Liberty Financial. Source: TradingView.

However, these conflicts of interest are not just limited to Sun’s investment.

Zhao could also benefit from an agreement. In 2023, he pleaded guilty to federal charges for failing to implement adequate anti-money-laundering measures at Binance.

Following his plea, Zhao resigned as Binance’s CEO. Motive-driven speculations point toward the possibility of a potential presidential pardon.

For Massad, maneuvers like these are natural when a president directly involves himself in crypto ventures.

“I think there is a huge risk of conflicts of interest and corruption by virtue of the President and people associated with him selling crypto assets—whether that’s through World Liberty Financial or the meme coins. It creates the potential for ongoing conflicts, because people who might want to curry favor with the administration could buy the coins,” Massad told BeInCrypto.

All the while, Trump benefits his crypto ventures every time he makes a pro-crypto announcement.

Is Trump Manipulating the Crypto Market?

A week into March, Trump signed an executive order to establish a Crypto Strategic Reserve and a US Digital Asset Stockpile. In his original announcement, Trump said the reserve would include Bitcoin, Ethereum, and altcoins like XRP, ADA, and SOL.

The crypto market responded immediately, with all five cryptocurrencies posting strong gains. Yet, Trump’s announcement quickly raised concerns over potential market manipulation.

With Bitcoin, Ethereum, and XRP in its treasury, WLF’s holdings grew in value as those assets appreciated. This growth could have boosted investor confidence, leading to higher demand for WLF tokens.

The crypto market’s overall surge and attention to Trump-related projects also generated greater investor interest in WLF, contributing to its price appreciation.

Meanwhile, Trump’s meme coin surged following the President’s reserve announcement. While TRUMP’s price stood at $13.55, with a trading volume of almost $1.2 billion on March 2, those numbers surged to $17.46 and $3.6 billion, respectively, following the news a day later.

On March 4, TRUMP’s price and trading volume plummeted below the numbers they registered only two days earlier.

“I think the meme coins have looked like a classic pump-and-dump scheme or money grab. I don’t think the issue should be, why not let people invest in these things if they want to? Of course they should have the right to invest in whatever they want. The issue is the propriety of the President of the United States selling things that capitalize on his being the President,” said Massad.

Even Ethereum Co-Founder Vitalik Buterin touched on the damaging effects of political meme coins in a social media post published five days after TRUMP’s launch.

“Now is the time to talk about the fact that large-scale political coins cross a further line: they are not just sources of fun, whose harm is at most contained to mistakes made by voluntary participants, they are vehicles for unlimited political bribery, including from foreign nation states,” Buterin said.

There is perhaps an analogy with weed here.

Ten years ago, to many weed represented freedom, and rebellion against sclerotic old order that denied self-sovereignty over our bodies. Then, weed became legalized, and “official”.

On that day, I remember my personal interest in weed…

Given Trump’s active participation in the crypto industry over the past several months, a vital question remains: Why hasn’t Trump been held accountable over these apparent conflicts of interest?

The answer remains short and bitter: He can’t be.

Can Trump Be Held Accountable?

The potential conflicts of interest arising from Donald Trump’s involvement in the cryptocurrency industry have drawn the attention of various political figures, particularly those focused on government ethics and oversight.

US Senator Elizabeth Warren has been the most vocal opponent of Trump’s dealings in the crypto industry.

“I write today to request information about how you, as President Trump’s ‘Crypto Czar,’ have addressed your conflicts of interest, and how you will prevent the President and other private individuals from directly profiting off of the Trump Administration’s efforts to selectively pump the value of certain crypto assets, drop crypto asset-related enforcement actions, and deregulate the crypto asset industry. These actions have the potential to benefit billionaire investors, Trump Administration insiders, and speculators at the expense of middle-class families,” Elizabeth Warren wrote.

However, not much else can be done beyond letters that demand responses and clarifications from the Trump administration.

The Legal Loophole

US Presidents are largely exempted from conflict of interest provisions. This exemption has been based on legal interpretations that argue these laws could impede the President’s ability to fulfill their constitutional duties.

“The problem is, the POTUS is not subject to the conflict-of-interest laws that apply to most other executive branch officeholders. There is the Foreign Emoluments Clause in the Constitution, which prohibits accepting gifts from foreign countries. There’s also a domestic clause that prohibits accepting gifts from the government. But beyond that, he’s not subject to the usual conflict-of-interest standards. So, it’s unfortunate that we don’t have those standards applicable to a president. I think, had any other president done these things, there would be far more outrage,” Massad told BeInCrypto.

Given the legal circumstances, public scrutiny and political pressure are the best ways to hold a president accountable for potential conflicts of interest.

Yet, despite the legal exemptions for sitting presidents, the ethical implications of Trump’s crypto dealings remain undeniable.

As the lines between political power and personal profit continue to blur, the necessity for clear ethical standards, even without legal mandates, becomes increasingly urgent.

Failing to do so might erode public trust in the crypto industry, generating potentially irreversible consequences.

The recent price action of Hedera (HBAR) shows a sharp decline of 11% over the last three days. The altcoin is moving away from Bitcoin’s (BTC) orbit, reflecting a shift in market sentiment and weakening investor confidence.

HBAR is now vulnerable to further decline, with worsening market conditions fueling outflows.

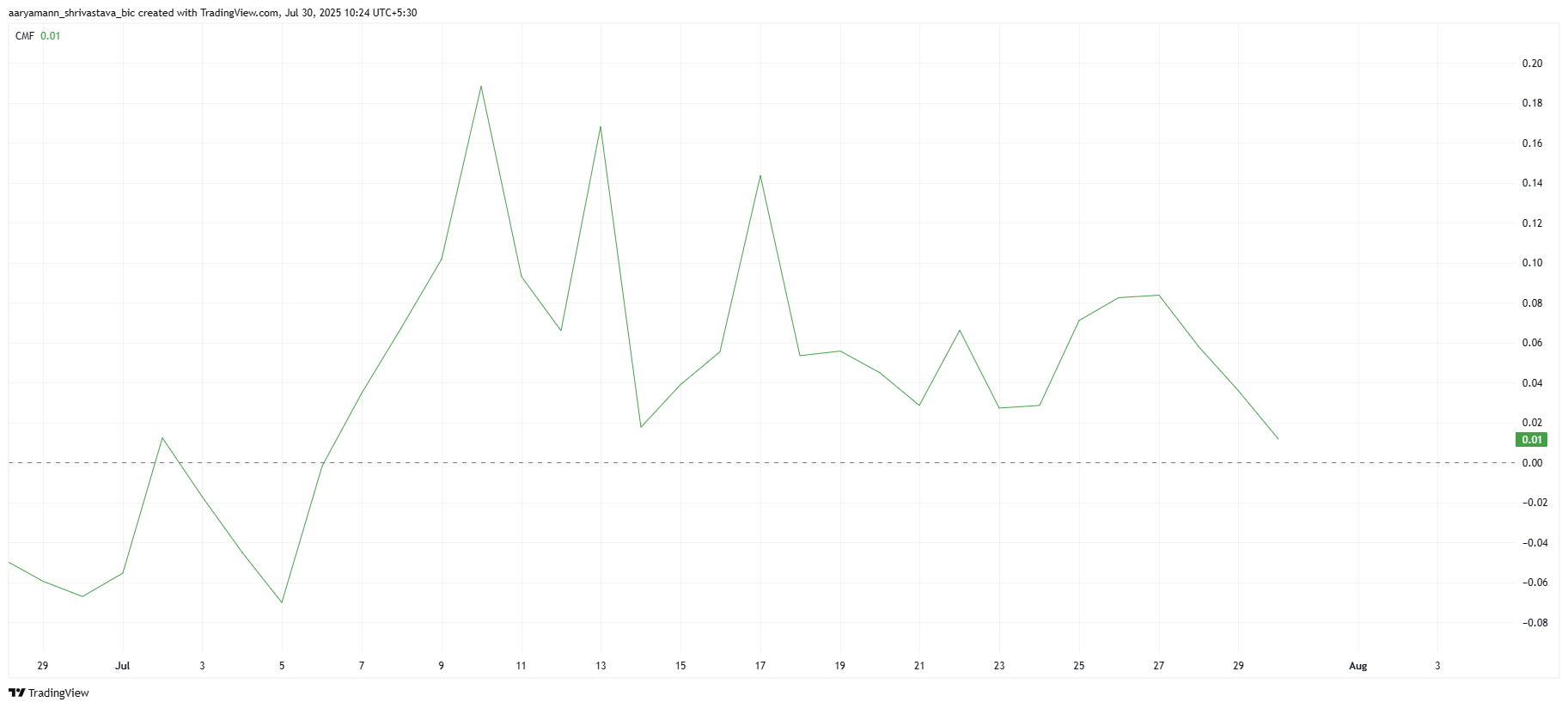

HBAR Investors Pull Back

The Chaikin Money Flow (CMF) for HBAR is currently sitting at a near 4-week low, close to the zero line. This suggests that investor outflows are dominating, with a significant shift from accumulation to selling. A drop below the zero line on the CMF would confirm that selling pressure is overwhelming the buying interest.

The current market sentiment is characterized by investor uncertainty. The weakening CMF reading highlights the lack of confidence in HBAR’s price potential in the near term. As HBAR faces these outflows, the altcoin could face a steeper decline.

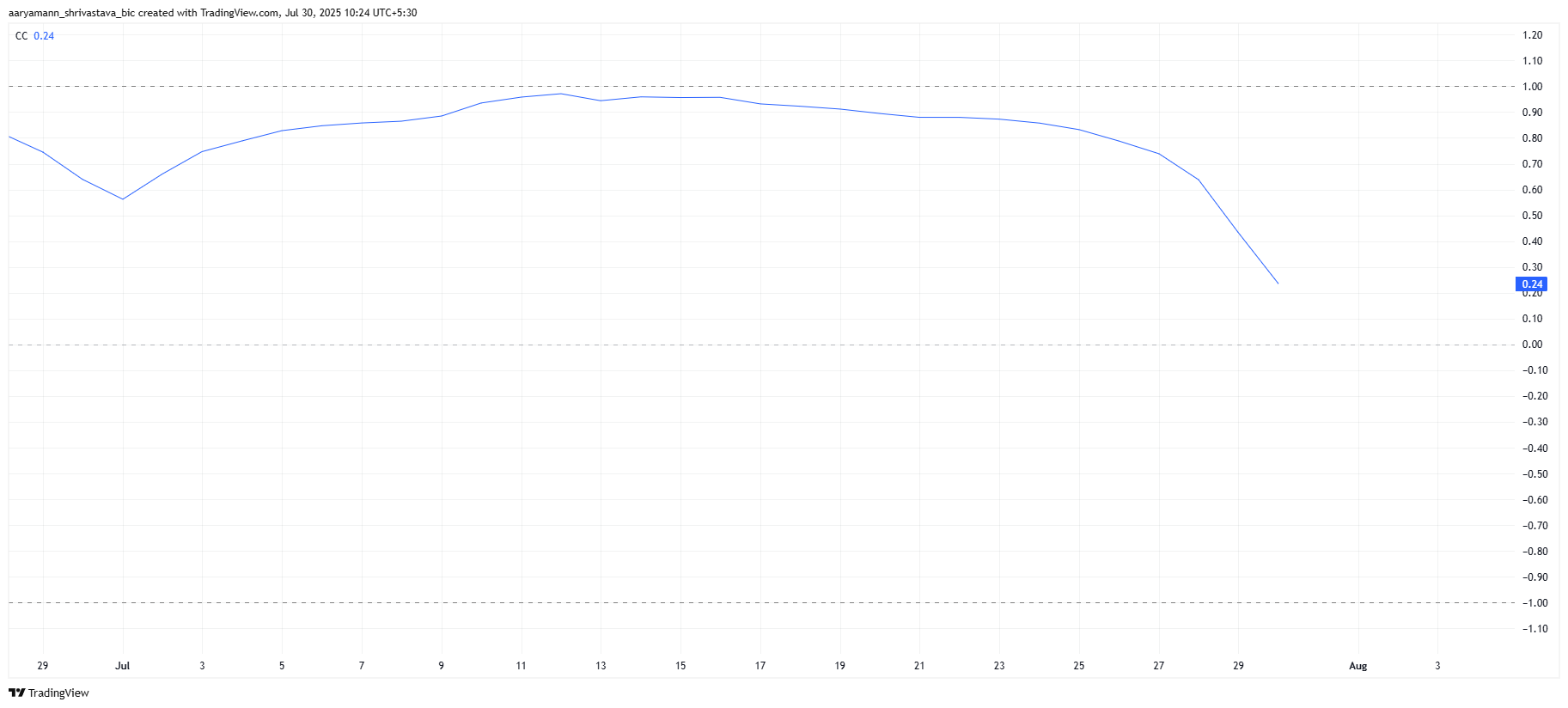

The broader market momentum for HBAR is heavily influenced by its correlation with Bitcoin. Currently, the correlation between HBAR and BTC is at a near 2-month low. This weakened correlation is a double-edged sword for HBAR as it could benefit from Bitcoin’s price drop, but any rally in BTC could negatively impact HBAR’s price.

The diminished connection to Bitcoin leaves HBAR more exposed to independent price action. With investor sentiment shifting and external market factors playing a larger role, HBAR’s price might experience more ups and downs, depending on the direction BTC takes.

Currently trading at $0.258, HBAR is in a vulnerable position after the recent 11% drop. The altcoin is sitting just above key support levels, and further decline is possible. A drop to the $0.236 support level seems likely, especially with the current market conditions and investor sentiment.

If the downward trend persists, HBAR could continue to consolidate between $0.236 and $0.276. These price levels may provide some stability, but they also represent areas of significant resistance. A prolonged consolidation phase could trap HBAR within this range, with little upward movement in the short term.

However, if market conditions reverse, HBAR might manage to reclaim the $0.276 level as support. This would open the door for a potential price surge toward $0.300. Whether it breaches this resistance remains uncertain, but a shift in sentiment could drive HBAR toward higher levels.

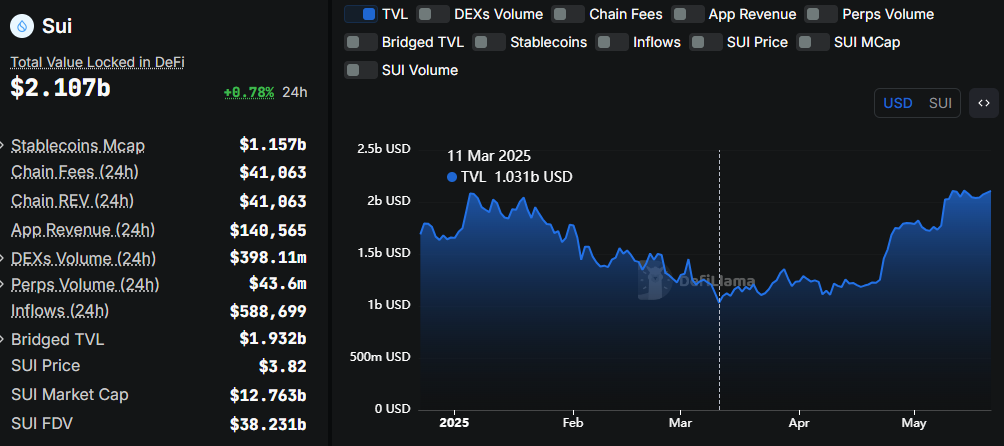

Sui Network (SUI) has hit a new milestone, with its total value locked (TVL) surging to new highs of over $2.1 billion.

This explosive growth is due to strong stablecoin inflows and heightened market momentum fueled by its recent partnership with tech giant Microsoft.

Sui TVL Reaches $2.1 Billion, What Is Driving The Surge?

Data on DefiLlama shows Sui TVL stood at $2.107 billion as of this writing. It is up by over 104% since its yearly lows of $1.031 billion recorded in March, with the growth signaling increasing user participation, market confidence, protocol growth, and liquidity.

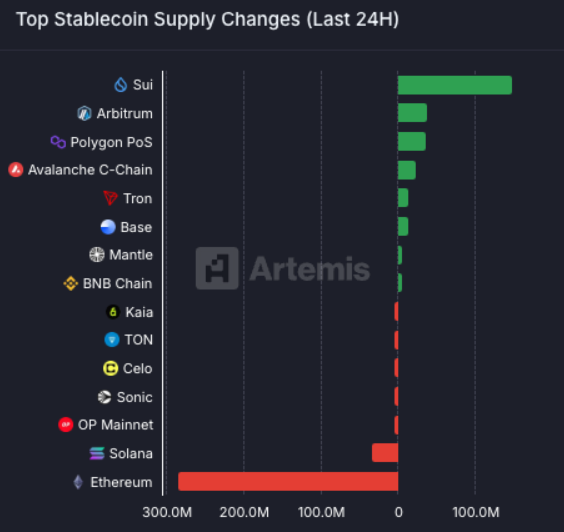

In the same way, data on Artemis shows that on Tuesday, the Sui Network led all blockchains in stablecoin inflows over the past 24 hours. Specifically, the total stablecoin supply on the network exceeded the $1 billion mark.

“Sui Network tops the charts with $148 million net stablecoin inflows in the past 24hrs,” wrote Adeniyi Abiodun, Mysten Labs co-founder and CPO, in a Tuesday post.

Sui blockchain led stablecoin flows on May 20. Source: Adeniyi on X

Mysten Labs is the creator of the Sui blockchain, a Layer 1 platform focused on high throughput and low latency.

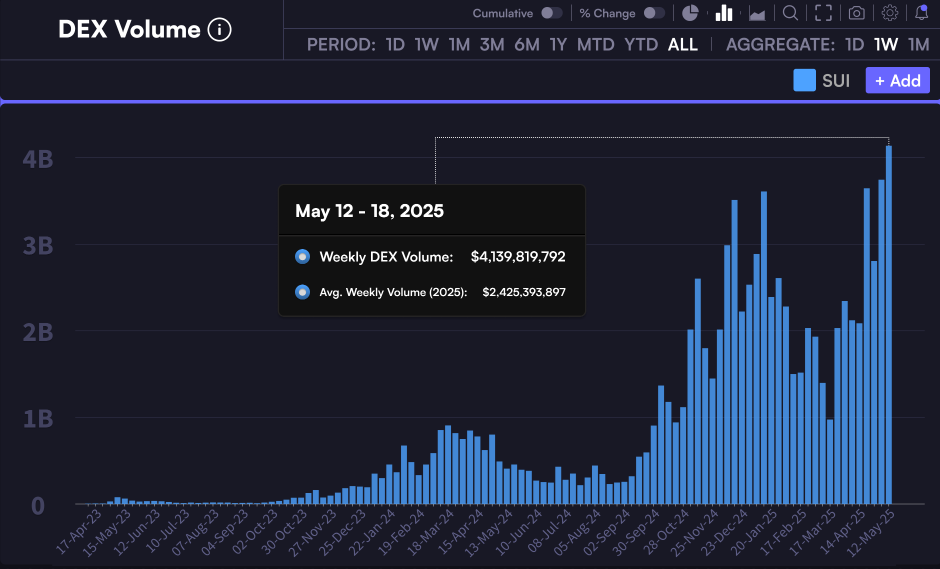

Meanwhile, the volume of weekly decentralized exchange (DEX) has also reached new highs. This suggests a sharp uptick in user activity and liquidity across the Sui ecosystem.

“Sui hits new all-time high in weekly DEX volume,” on-chain analyst ToreroRomero observed in a post.

A broader narrative of enterprise adoption underpins this bullish market structure. During Microsoft’s Build conference, Sui was named one of the first blockchains to integrate with Microsoft Fabric via data indexing platform Space and Time.

Sui Integrates with Microsoft Fabric

This integration enables Microsoft’s vast developer ecosystem to access Sui’s full-chain history in real-time. The move paves the way for a new wave of institutional-grade blockchain applications.

“Just announced at MSBuild: Space and Time indexed blockchain data will be integrated with Microsoft Fabric. As part of the integration, Microsoft developers will be able to access Space and Time indexed data from Bitcoin, Sui Network, and Ethereum through Fabric,” said Space and Time in a statement.

MySten Labs executive Adeniyi Abiodun emphasized the long-term vision, projecting Sui blockchain’s growth in the next five years.

“Mark my words, by 2030, in-game ownership will be baked into every major game out there and Sui Network will be the backbone making it all happen,” Abiodun predicted.

Technical market signals also reflect the bullish fundamentals. According to Rose Premium Signals, SUI’s price action remains strong despite a current pullback.

“Sui is holding its Inverse Head & Shoulders breakout. After breaking the neckline around $3.65–$3.75, the price pushed up to $3.94 and is now pulling back, retesting the breakout zone….Targets remain: 1st Target: $4.76, 2nd Target: $5.67. Holding above $3.65–$3.70 confirms strength,” they wrote on X.

At the time of writing, SUI is trading around $3.87, down by 0.22% in the last 24 hours. According to the analysts, however, a drop below $3.60 could invalidate the pattern, but for now, sentiment remains decisively positive.

Investor interest in Sui continues to grow, with notable figures such as macro investor Raoul Pal stating that over 70% of his portfolio is currently allocated to Sui.

Here’s my recent talk at Sui Basecamp in Dubai—Enjoy!

00:00 – PALvatar introduces the episode 01:04 – Reframing the macro fear narrative 01:26 – The Everything Code and liquidity 01:51 – Debt cycles and macro structure 02:10 – Demographics, debt, and GDP 02:38 – Aging… pic.twitter.com/iIBHkW6d2O

BNB (@cz_binance)

BNB (@cz_binance)