After Bitcoin (BTC), Ethereum (ETH) has emerged as the next institutional favorite. According to Geoff Kendrick, Head of Digital Assets Research at Standard Chartered, corporate treasuries have purchased 1% of all ETH in circulation since the beginning of June.

This highlights the growing appetite among firms to increase their ETH exposure. Kendrick also shared with BeInCrypto that these corporate treasuries could eventually hold 10% of all ETH.

Institutions Aggressively Accumulate ETH in June

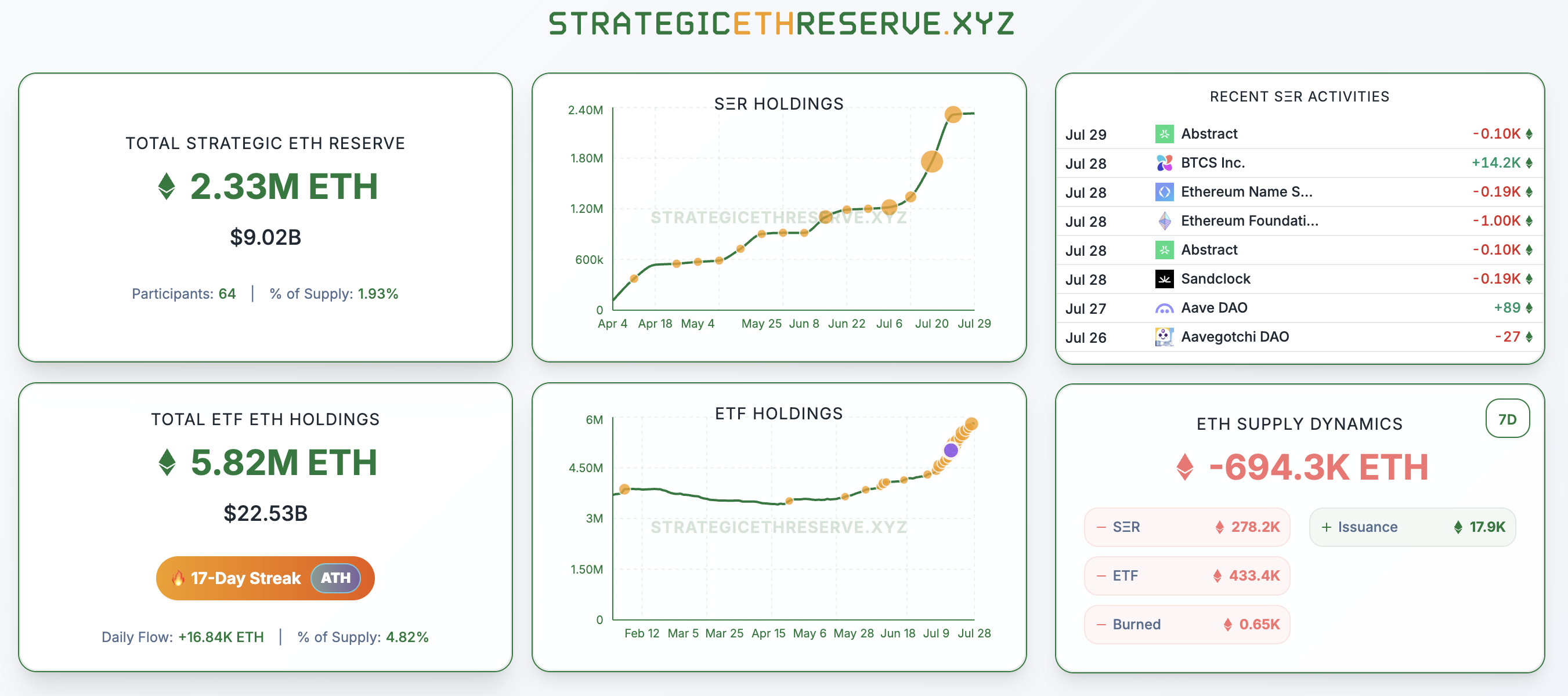

BeInCrypto previously reported that firms are accelerating their efforts to acquire ETH as part of their treasury strategy. According to the latest data, the Strategic ETH Reserve, which tracks entities holding Ethereum in their treasuries, now totals 2.33 million ETH, valued at over $9 billion.

These holdings, distributed among 64 entities, account for 1.93% of Ethereum’s supply. This marks a significant rise from the 789,705 ETH held in mid-May. In just over two months, the entities’ ETH holdings have surged by approximately 195%.

Notably, 113,000 ETH (approximately $409 million) is held by companies that revealed their positions for the first time this quarter.

Meanwhile, a few firms stand out for their massive holdings. For instance, BitMine Immersion Technologies, which initially committed $250 million to an ETH reserve, has already topped over $2 billion in ETH holdings in a month.

Standard Chartered’s Geoff Kendrick highlighted that public companies with digital assets on their balance sheets have acquired 1% of ETH’s circulating supply in just two months. What’s particularly noteworthy is the pace of acquisition—this rate is double that of Bitcoin purchases by corporate treasuries.

“This buying was almost as strong as ETH ETF buying, which has also been the strongest on record. We expect ETH treasury companies to eventually own 10% of all ETH, a 10x increase from here,” Kendrick told BeInCrypto.

He stressed that in terms of flows, ETH treasury companies are becoming more important than their BTC counterparts.

“ETH treasury companies make more sense than their BTC equivalents due to staking yield, DeFi leverage. And from a regulatory arbitrage perspective, they make more sense than their BTC equivalents, too,” he said.

Why Corporate Firms Are Increasing Their Ethereum Holdings?

The executive explained that corporate treasury investments in ETH are appealing due to the financial system’s inefficiencies, which are largely driven by regulatory barriers.

Additionally, ETH treasuries can benefit from staking rewards and leverage opportunities within decentralized finance (DeFi). These are currently unavailable through US Ethereum ETFs.

Kendrick also noted that the momentum has contributed to ETH’s latest price rally. BeInCrypto Markets data showed that the price appreciated 56.9% over the past month, and peaked at highs last seen many months ago.

“ETH has significantly outperformed BTC since ETH treasury companies took hold in early June, with the ETH-BTC cross up from an April low of 0.018 to 0.032 now. Buying by these companies, along with the best period for ETH ETFs on record, has certainly contributed to those gains. If the flows can continue, ETH may be able to break above the key USD 4,000 level (our current end-2025 forecast),” Kendrick disclosed to BeInCrypto.

The metrics used to measure outcomes can be misleading when evaluating blockchain performance. As more blockchain networks emerge, the public needs clear, efficiency-focused metrics, rather than exaggerated claims, to differentiate between them.

In a conversation with BeInCrypto, Taraxa Co-Founder Steven Pu explained that it’s becoming increasingly difficult to compare blockchain performance accurately because many reported metrics rely on overly optimistic assumptions rather than evidence-based results. To combat this wave of misrepresentation, Pu proposes a new metric, which he calls TPS/$.

Why Does the Industry Lack Reliable Benchmarks?

The need for clear differentiation is growing with the increasing number of Layer-1 blockchain networks. As various developers promote the speed and efficiency of their blockchains, relying on metrics that distinguish their performance becomes indispensable.

However, the industry still lacks reliable benchmarks for real-world efficiency, instead relying on sporadic sentimental waves of hype-driven popularity. According to Pu, misleading performance figures currently saturate the market, obscuring true capabilities.

“It’s easy for opportunists to take advantage by driving up over-simplified and exaggerated narratives to profit themselves. Every single conceivable technical concept and metric has at one time or another been used to hype up many projects that don’t really deserve them: TPS, finality latency, modularity, network node count, execution speed, parallelization, bandwidth utilization, EVM-compatibility, EVM-incompatibility, etc.,” Pu told BeInCrypto.

Pu focused on how some projects exploit TPS metrics, using them as marketing tactics to make blockchain performance sound more appealing than it might be under real-world conditions.

Examining the Misleading Nature of TPS

Transactions per second, more commonly known as TPS, is a metric that refers to the average or sustained number of transactions that a blockchain network can process and finalize per second under normal operating conditions.

However, it often misleadingly hypes projects, offering a skewed view of overall performance.

“Decentralized networks are complex systems that need to be considered as a whole, and in the context of their use cases. But the market has this horrible habit of over-simplifying and over-selling one specific metric or aspect of a project, while ignoring the whole. Perhaps a highly centralized, high-TPS network does have its uses in the right scenarios with specific trust models, but the market really has no appetite for such nuanced descriptions,” Pu explained.

Pu indicates that blockchain projects with extreme claims on single metrics like TPS may have compromised decentralization, security, and accuracy.

“Take TPS, for example. This one metric masks numerous other aspects of the network, for example, how was the TPS achieved? What was sacrificed in the process? If I have 1 node, running a WASM JIT VM, call that a network, that gets you a few hundred thousand TPS right off the bat. I then make 1000 copies of that machine and call it sharding, now you start to get into the hundreds of millions of ‘TPS’. Add in unrealistic assumptions such as non-conflict, and you assume you can parallelize all transactions, then you can get “TPS” into the billions. It’s not that TPS is a bad metric, you just can’t look at any metric in isolation because there’s so much hidden information behind the numbers,” he added.

The Taraxa Co-founder revealed the extent of these inflated metrics in a recent report.

The Significant Discrepancy Between Theoretical and Real-World TPS

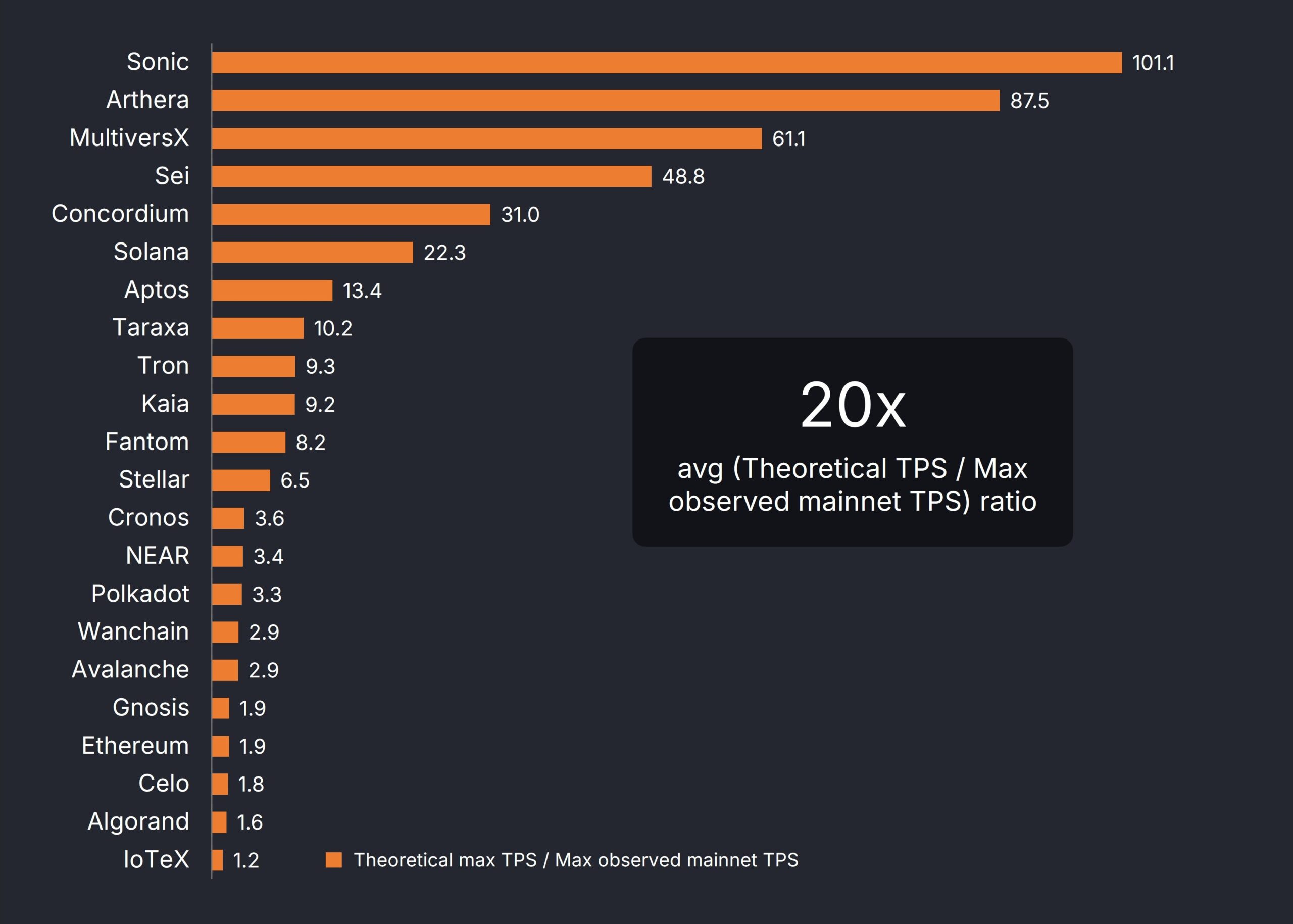

Pu sought to prove his point by determining the difference between the maximum historical TPS realized on a blockchain’s mainnet and the maximum theoretical TPS.

Of the 22 permissionless and single-shard networks observed, Pu found that, on average, there was a 20-fold gap between theory and reality. In other words, the theoretical metric was 20 times higher than the maximum observed mainnet TPS.

Taraxa Co-founder finds 20x difference between the Theoretical TPS and the Max Observed Mainnet TPS. Source: Taraxa.

“Metric overestimations (such as in the case of TPS) are a response to the highly speculative and narrative-driven crypto market. Everyone wants to position their project and technologies in the best possible light, so they come up with theoretical estimates, or conduct tests with wildly unrealistic assumptions, to arrive at inflated metrics. It’s dishonest advertising. Nothing more, nothing less,” Pu told BeInCrypto.

Looking to counter these exaggerated metrics, Pu developed his own performance measure.

Introducing TPS/$: A More Balanced Metric?

Pu and his team developed the following: TPS realized on mainnet / monthly $ cost of a single validator node, or TPS/$ for short, to fulfill the need for better performance metrics.

This metric assesses performance based on verifiable TPS achieved on a network’s live mainnet while also considering hardware efficiency.

The significant 20-fold gap between theoretical and actual throughput convinced Pu to exclude metrics based solely on assumptions or lab conditions. He also aimed to illustrate how some blockchain projects inflate performance metrics by relying on costly infrastructure.

“Published network performance claims are often inflated by extremely expensive hardware. This is especially true for networks with highly centralized consensus mechanisms, where the throughput bottleneck shifts away from networking latency and into single-machine hardware performance. Requiring extremely expensive hardware for validators not only betrays a centralized consensus algorithm and inefficient engineering, it also prevents the vast majority of the world from potentially participating in consensus by pricing them out,” Pu explained.

Pu’s team located each network’s minimum validator hardware requirements to determine the cost per validator node. They later estimated their monthly cost, paying particular attention to their relative sizing when used to compute the TPS per dollar ratios.

“So the TPS/$ metric tries to correct two of the perhaps most egregious categories of misinformation, by forcing the TPS performance to be on mainnet, and revealing the inherent tradeoffs of extremely expensive hardware,” Pu added.

Pu stressed considering two simple, identifiable characteristics: whether a network is permissionless and single-sharded.

Permissioned vs. Permissionless Networks: Which Fosters Decentralization?

A blockchain’s degree of security can be unveiled by whether it operates under a permissioned or permissionless network.

Permissioned blockchains refer to closed networks where access and participation are restricted to a predefined group of users, requiring permission from a central authority or trusted group to join. In permissionless blockchains, anyone is allowed to participate.

According to Pu, the former model is at odds with the philosophy of decentralization.

“A permissioned network, where network validation membership is controlled by a single entity, or if there is just a single entity (every Layer-2s), is another excellent metric. This tells you whether or not the network is indeed decentralized. A hallmark of decentralization is its ability to bridge trust gaps. Take decentralization away, then the network is nothing more than a cloud service,” Pu told BeInCrypto.

Attention to these metrics will prove vital over time, as networks with centralized authorities tend to be more vulnerable to certain weaknesses.

“In the long term, what we really need is a battery of standardized attack vectors for L1 infrastructure that can help to reveal weaknesses and tradeoffs for any given architectural design. Much of the problems in today’s mainstream L1 are that they make unreasonable sacrifices in security and decentralization. These characteristics are invisible and extremely hard to observe, until a disaster strikes. My hope is that as the industry matures, such a battery of tests will begin to organically emerge into an industry-wide standard,” Pu added.

Meanwhile, understanding whether a network employs state-sharding versus maintaining a single, sharded state reveals how unified its data management is.

State-Sharding vs. Single-State: Understanding Data Unity

In blockchain performance, latency refers to the time delay between submitting a transaction to the network, confirming it, and including it in a block on the blockchain. It measures how long it takes for a transaction to be processed and become a permanent part of the distributed ledger.

Identifying whether a network employs state-sharding or a single-sharded state can reveal much about its latency efficiency.

State-sharded networks divide the blockchain’s data into multiple independent parts called shards. Each shard operates somewhat independently and doesn’t have direct, real-time access to the complete state of the entire network.

By contrast, a non-state-sharded network has a single, shared state across the entire network. All nodes can access and process the same complete data set in this case.

Pu noted that state-sharded networks aim to increase storage and transaction capacity. However, they often face longer finality latencies due to a need to process transactions across multiple independent shards.

He added that many projects adopting a sharding approach inflate throughput by simply replicating their network rather than building a truly integrated and scalable architecture.

“A state-sharded network that doesn’t share state, is simply making unconnected copies of a network. If I take a L1 network and just make 1000 copies of it running independently, it’s clearly dishonest to claim that I can add up all the throughput across the copies together and represent it as a single network. There are architectures that actually synchronize the states as well as shuffle the validators across shards, but more often than not, projects making outlandish claims on throughput are just making independent copies,” Pu said.

Based on his research into the efficiency of blockchain metrics, Pu highlighted the need for fundamental shifts in how projects are evaluated, funded, and ultimately succeed.

What Fundamental Shifts Does Blockchain Evaluation Need?

Pu’s insights present a notable alternative in a Layer-1 blockchain space where misleading performance metrics increasingly compete for attention. Reliable and effective benchmarks are essential to counter these false representations.

“You only know what you can measure, and right now in crypto, the numbers look more like hype-narratives than objective measurements. Having standardized, transparent measurements allows simple comparisons across product options so developers and users understand what it is they’re using, and what tradeoffs they’re making. This is a hallmark of any mature industry, and we still have a long way to go in crypto,” Pu concluded.

Adopting standardized and transparent benchmarks will foster informed decision-making and drive genuine progress beyond merely promotional claims as the industry matures.

Murad Mahmudov, a well-known investor and meme coin proponent, predicts that older meme coins will continue to outperform their newer counterparts.

This forecast comes amid a broader bull run, where meme coins as a whole are benefiting from renewed investor enthusiasm.

Why Investors Are Betting Big on Older Meme Coins

According to CoinGecko data, the overall meme coin market capitalization has increased 17.33% over the past month. Among the top coins, Dogecoin (DOGE), Floki (FLOKI), and Pudgy Penguins (PENGU) have experienced 22.3%, 46.4%, and 116.6% appreciation, respectively, contributing greatly to the overall growth.

Furthermore, over the past day alone, the total market cap of meme coins has increased 4.9% to nearly $70 billion. Amid this market surge, a pseudonymous analyst, “boot”, stressed that investors are showing a growing preference for established mid- and large-cap meme coins over newly launched tokens.

“The best traders I know have pivoted entirely to mid/high-cap memes. Very few of these tokens launched in 2025. They won’t touch a new launch, regardless of the narrative. Do with that information what you will,” the analyst posted.

Moreover, he added that coins with large market caps are relatively safer investments compared to smaller, newer, or low-market-cap tokens.

Prominent crypto investor Murad echoed this sentiment in a reply to Boot’s post. The investor forecasts that coins launched in 2023 and select tokens from 2024 will maintain stronger performance.

“2023 and some 2024 coins will continue to outperform,” Murad said.

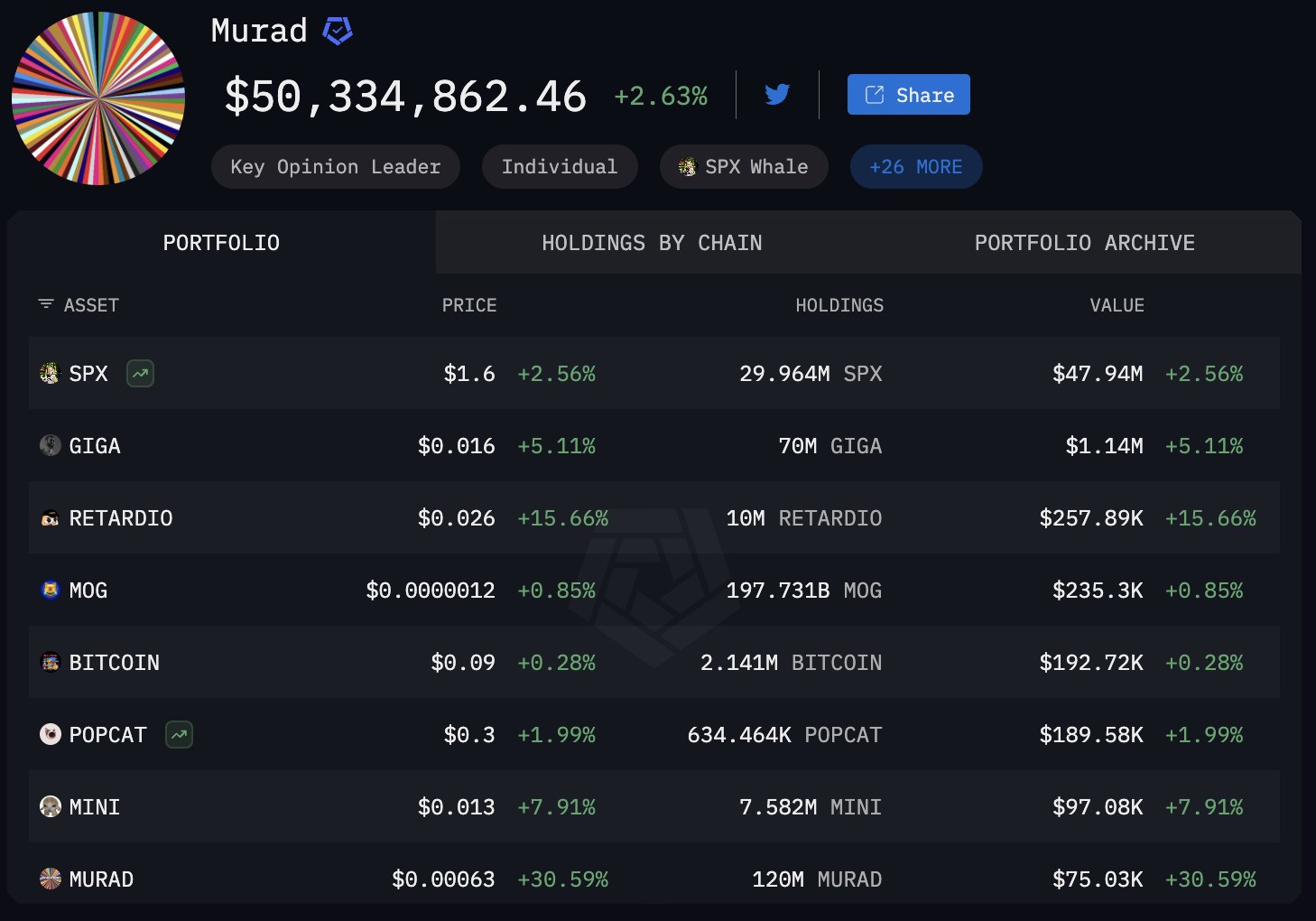

His confidence in older tokens aligns with his investment portfolio, which recently neared record highs, as reported by BeInCrypto. Data from Arkham Intelligence, a blockchain analytics platform, showed that Murad’s largest holdings by value, SPX6900 (SPX), Gigachad (GIGA), and Retardio (RETARDIO), are all older meme coins launched between 2023 and 2024.

But why would investors favor some coins over others? Analyst Ignas pointed out that this all comes down to the intention behind most token launches.

He said that many founders create tokens with their own personal gain in mind, not the community’s. In addition, many tokens lack excitement and purpose.

“When I buy a token, I want to DREAM BIG. Yet most projects focus on selling their features rather than their grand ambitions. Token is there to make your community dream,” he stated.

Nonetheless, another pseudonymous analyst, Xero, emphasized that investors are favoring older meme coins right now because the market is likely still in Phase 1 of the meme coin cycle. In this early stage of a bull run, capital tends to flow into established tokens before rotating to other meme coins.

“It think that’s because it’s phase 1. Before we have runners again we need multiple ath on older coins,” the analyst replied.

Therefore, for now, Murad’s prediction and the broader trader pivot suggest a strategic preference for older coins. Still, time will tell whether investors will continue to favor them or shift their strategies.

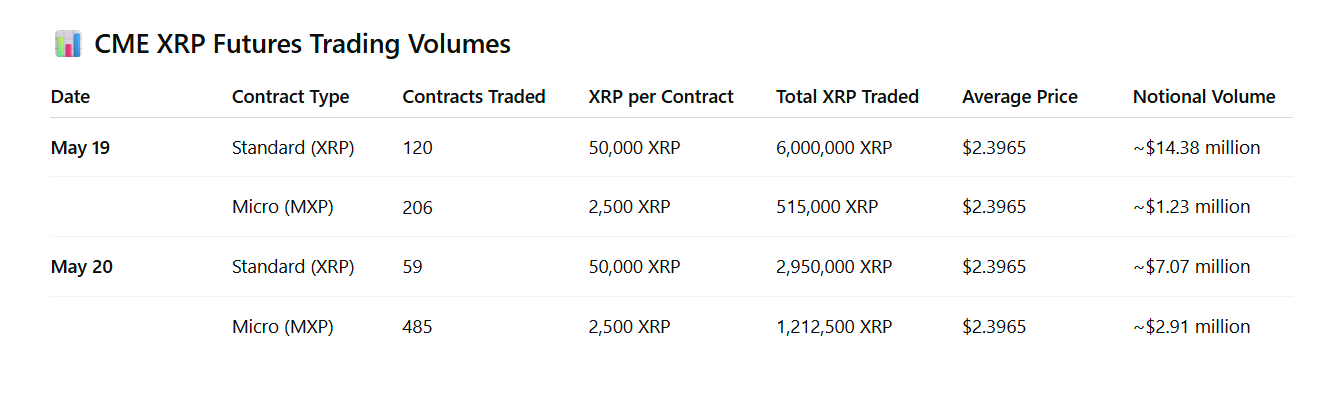

XRP futures trading on CME Group has surged to a combined $25.6 million in notional volume within its first two days of launch. It marks a strong debut for the altcoin’s entry into regulated derivatives markets. Meanwhile, XRP continues to trade below $2.50, dropping 7% in the past week.

According to official CME data and corroborating reports, 120 standard and 206 micro contracts were traded on May 19, totaling approximately 6.5 million XRP.

On May 20, the exchange logged 59 standard and 485 micro contracts, adding another 4.1 million XRP to the tally.

So, using XRP’s current market price of $2.39, the total trading volume across both days equals approximately $25.6 million.

XRP Futures Notional Volume on CME. Source: CME Group

This volume positions XRP’s debut ahead of other altcoin launches on CME. Solana (SOL) futures, which debuted in March 2025, recorded $12.3 million in first-day notional volume.

Futures Mirror XRP Spot Price, Hint at Stable Outlook

CME’s XRP futures are cash-settled and based on the CME CF XRP-Dollar Reference Rate. This is updated daily at 11 am Eastern Time.

This structure means the futures are pegged closely to the spot market. With XRP currently trading at $2.39, the futures contracts are not reflecting a premium or discount. This suggests traders expect price stability in the short term.

So far, there is no indication of strong bullish or bearish sentiment among futures participants. This could reflect broader market indecision or simply the fact that participants are using the contracts for hedging rather than speculation.